Question

Answer

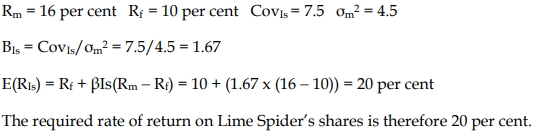

Using the Capital Asset Pricing Model (CAPM):

Step 1: Calculate Beta (β):

β = CovLs / σ²m

= 7.5 / 4.5

= 1.67

Step 2: Apply CAPM formula:

E(RLs)=Rf+β(Rm−Rf)E(R_{Ls}) = Rf + β (Rm – Rf)

= 10% + 1.67 × (16% – 10%)

= 10% + 1.67 × 6%

= 10% + 10.02%

= 20.02%

Conclusion:

The required rate of return for Lime Spider Ltd’s shares is 20%.

OR