Question

Answer

MAPUTO NIGERIA LIMTED

PROCESS 2 ACCOUNTS

a

i)

PROCESS 3 ACCOUNTS

ii)

b) NORMAL LOSS ACCOUNT

c) ABNORMAL LOSS ACCOUNT

ABNORMAL GAIN ACCOUNT

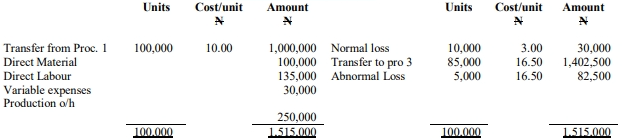

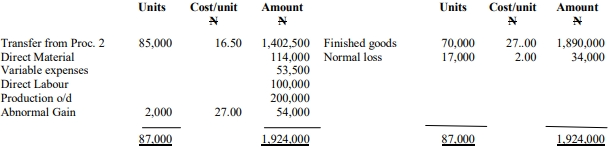

MAPUTO NIGERIA LIMITED manufactures its product through three processes. The following data relates to Process 2 and Process 3 for the month of October:

| Cost Components | Process 2 (N) | Process 3 (N) |

|---|---|---|

| Direct Materials | 100,000 | 114,000 |

| Direct Labour | 135,000 | 100,000 |

| Variable Expenses | 30,000 | 53,500 |

| Production Overhead | 250,000 | 200,000 |

Required:

a. Prepare Process 2 and Process 3 accounts (16 Marks)

b. Prepare the Normal Loss account (2 Marks)

c. Prepare the Abnormal Gain account (2 Marks)

MAPUTO NIGERIA LIMTED

PROCESS 2 ACCOUNTS

a

i)

PROCESS 3 ACCOUNTS

ii)

b) NORMAL LOSS ACCOUNT

c) ABNORMAL LOSS ACCOUNT

ABNORMAL GAIN ACCOUNT

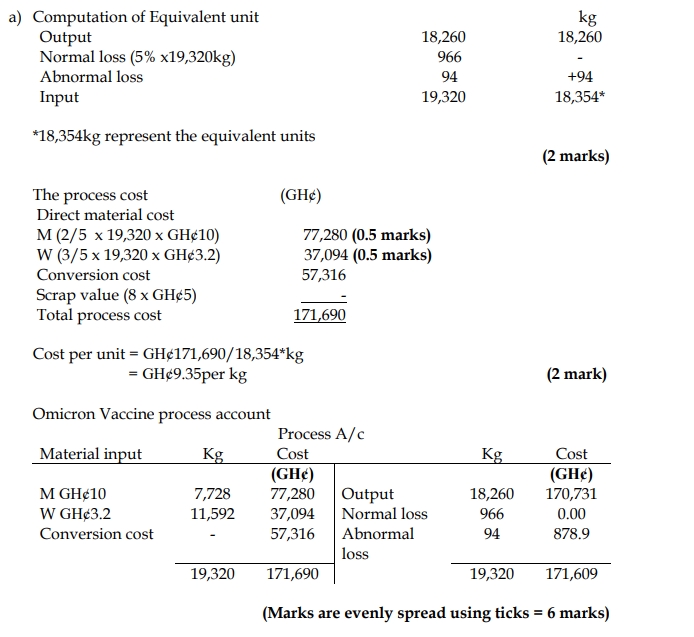

a) Adom Ltd manufactures Omicron vaccine for the treatment of COVID-19 in Africa. The manufacturing process uses two raw materials (M & W) which are mixed in the proportions (2:3). Materials are priced: M = GH¢10 per kg and W = GH¢3.2 per kg. Normal weight loss of 5% of material input is expected during the process, and material losses recorded in the manufacturing process have no saleable value. At the end of production, 18,260 kg of Omicron vaccine were manufactured from 19,320 kg of raw materials. Conversion costs in the period were GH¢57,316. There was no work in process at the beginning or end of the period.

Required:

Prepare the Process Account of the Omicron vaccine for the period. (10 marks)

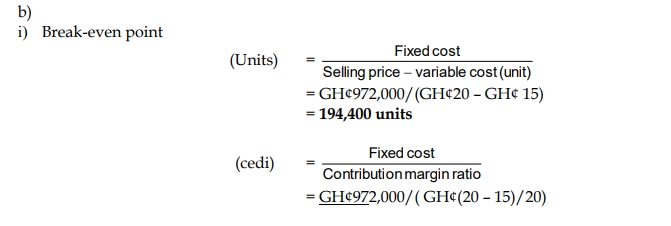

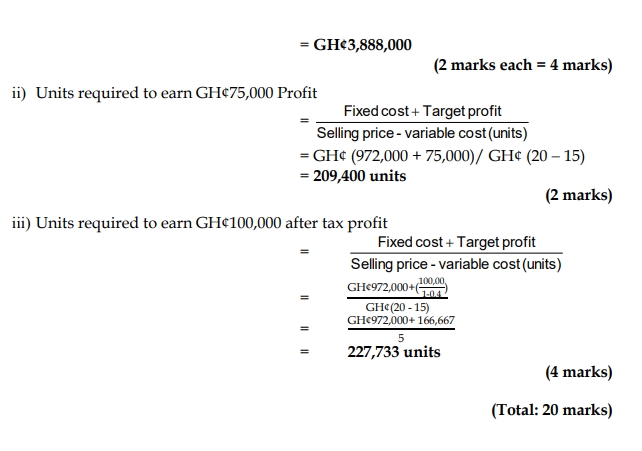

b) Manna Industries sold 150,000 units of its product at GH¢20 per unit. Variable costs are GH¢15 per unit (manufacturing cost of GH¢12 and selling expenses of GH¢3). Fixed costs are incurred uniformly throughout the year and amount to GH¢972,000, that is, manufacturing costs of GH¢600,000 and selling expenses of GH¢372,000.

Required:

i) Calculate the break-even point in units and Ghana cedis. (4 marks)

ii) Calculate the number of units that must be sold to earn an income of GH¢75,000 before income tax. (2 marks)

iii) Calculate the number of units that must be sold to earn an after-tax profit of GH¢100,000 if the income tax rate is 40%. (4 marks)

a) Frankadua Furniture Works located at Bomaa in the Ahafo Region has a rough estimate of the materials and labour cost of a set of living room furniture. It is expected that 8 cubic metres of timber, 6 cubic metres of foam and 12 square metres of fabric can be used. Glue, screws and other accessories will also cost GH¢80.

The Carpenters who will do the cutting, joining and finishing will use 35 hours. Since the company is fairly new, it will engage a tailor to sew the fabric to fit the sizes of the units of the chairs. For each set the tailor will charge GH¢150. Labour is paid at GH¢12 per hour plus a premium of GH¢5 per hour when the job requires more than 20 hours.

Timber is priced at GH¢25 per cubic metre, foam is GH¢20 per cubic metre while the fabric is GH¢15 per square metre. The Accountant has estimated overhead absorption rate of 20% on direct material cost.

Required:

i) Determine the prime cost of a set of living room furniture. (10 marks)

ii) Determine the full cost of a set of living room furniture. (5 marks)

b) Kempion Breweries Ltd has just commenced business in the alcoholic beverage sector of Ghana producing a local gin called Pitoo and is desirous of having a good grasp of its costs for product costing, valuation and pricing purposes.

Required:

State FOUR (4) features of a process costing system to be used by Kempion Breweries to arrive at the total cost of Pitoo. (5 marks)

a) i) Prime cost of the set of furniture:

| Description | Calculation | GH¢ |

|---|---|---|

| Timber | 8 cubic metres x GH¢25/m³ | 200 |

| Foam | 6 cubic metres x GH¢20/m³ | 120 |

| Fabric | 12 square metres x GH¢15/m² | 180 |

| Glue, screws, accessories | 80 | |

| Direct labour | 35 hours x GH¢12/hour + (15 hours x GH¢5/hour premium) | 420 |

| Direct expenses | Tailor charges | 150 |

| Total Prime Cost | 1,150 |

(10 marks)

ii) Full cost:

| Description | Calculation | GH¢ |

|---|---|---|

| Prime cost | From above | 1,150 |

| Overhead | 20% of direct material cost (GH¢500) | 100 |

| Total Full Cost | 1,250 |

(5 marks)

b) Features of a process costing system:

a) The following information has been extracted from the records of a company for the half-year ended 31 March 2021. A product, Capital Q, goes through two processes, X and Y:

Details relating to Process X for the period: Input units: 5,000 Finished units transferred to Process Y: 3,200 Closing WIP: 840 Normal losses: 10%

Normal losses have an estimated resale value of GH¢4 per unit.

Costs incurred during the period:

| GH¢ | |

|---|---|

| Direct materials | 31,250 |

| Direct labour | 21,200 |

| Overheads | 17,325 |

Abnormal Losses and Closing WIP had the following degrees of completion at the end of the period:

| Direct materials | Direct labour | Overheads | |

|---|---|---|---|

| Abnormal Losses | 100% | 80% | 50% |

| Closing WIP | 100% | 80% | 50% |

Required: Using the weighted average method: i) Compute the cost per unit for each of the element of costs. (5 marks)

b) Compute the value of the complete units transferred to Process Y. (5 marks)

c) Compute the value of the closing WIP. (5 marks)

d) Prepare Process X Account for the period. (5 marks)

a) i) Computation of the cost per unit for each element of cost:

| Item | Complete Unit | Closing WIP | Abnormal Loss | TEU | Total Cost (GH¢) | Cost/unit (GH¢) |

|---|---|---|---|---|---|---|

| Materials | 3,200 | 840 | 460 | 4,500 | 29,250 | 6.50 |

| Labour | 3,200 | 672 | 368 | 4,240 | 21,200 | 5.00 |

| Overheads | 3,200 | 420 | 230 | 3,850 | 17,325 | 4.50 |

| Total | 16.00 | |||||

| *GH¢29,250 = [31,250 – (GH¢4 x 500)] | ||||||

| (5 marks) |

b) Valuation of Complete Units: GH¢16 x 3,200 units = GH¢51,200 (5 marks)

c) Valuation of Closing WIP:

| GH¢ | |

|---|---|

| Materials (840 x GH¢6.50) | 5,460 |

| Labour (672 x GH¢5.00) | 3,360 |

| Overheads (420 x GH¢4.50) | 1,890 |

| Total | 10,710 |

| (5 marks) |

d) Process X Account:

| Units | Price | Amount (GH¢) | Units | Price | Amount (GH¢) |

|---|---|---|---|---|---|

| Materials | 5,000 | 31,250 | Normal Loss | 500 | 2,000 |

| Labour | 21,200 | Transfer to Y | 3,200 | 51,200 | |

| Overheads | 17,325 | Abnormal Loss | 460 | 5,865 | |

| WIP c/d | 840 | 10,710 | |||

| Total | 5,000 | 69,775 | Total | 5,000 | 69,775 |

| (5 marks) |

Valuation of Abnormal Loss:

| GH¢ | |

|---|---|

| Materials (460 x GH¢6.50) | 2,990 |

| Labour (368 x GH¢5.00) | 1,840 |

| Overheads (230 x GH¢4.50) | 1,035 |

| Total | 5,865 |

Take control of your business data with insight and in-depth understanding by taking this course.

Follow us on our social media and get daily updates.