- 20 Marks

Question

On 30 June 2019, the accounting records of Kofi, a sole trader, were partly destroyed by fire. The following list of assets, liabilities, and equity as at 30 June 2018 is available:

| Assets, Liabilities, and Equity | Amount (GH¢) |

|---|---|

| Plant and equipment – cost | 200,000 |

| – Accumulated depreciation | 72,000 |

| Office fixtures– cost | 50,000 |

| – Accumulated depreciation | 5,000 |

| Inventory | 30,500 |

| Trade receivables and prepayments – Note (iv) | 35,000 |

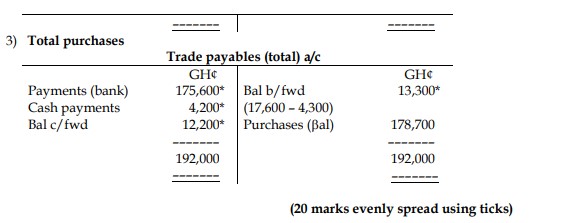

| Trade payables and accrued expenses – Note (iv) | 17,600 |

| Bank overdraft | 8,850 |

| Loan (10% interest per annum) | 95,000 |

| Capital | 117,050 |

The following summary of receipts and payments for the year to 30 June 2019 has been extracted from the bank statements:

| Receipts | Amount (GH¢) |

|---|---|

| Capital introduced | 22,000 |

| From credit customers | 427,500 |

| Payments | Amount (GH¢) |

|---|---|

| Cash drawings – Note (v) | 22,450 |

| Loan repayments – Note (vii) | 20,000 |

| To credit suppliers | 175,600 |

| Rent | 22,000 |

| Wages | 90,000 |

| Office expenses | 12,500 |

In preparing the statement of profit or loss and statement of financial position at 30 June 2019, the following further information is relevant:

Notes

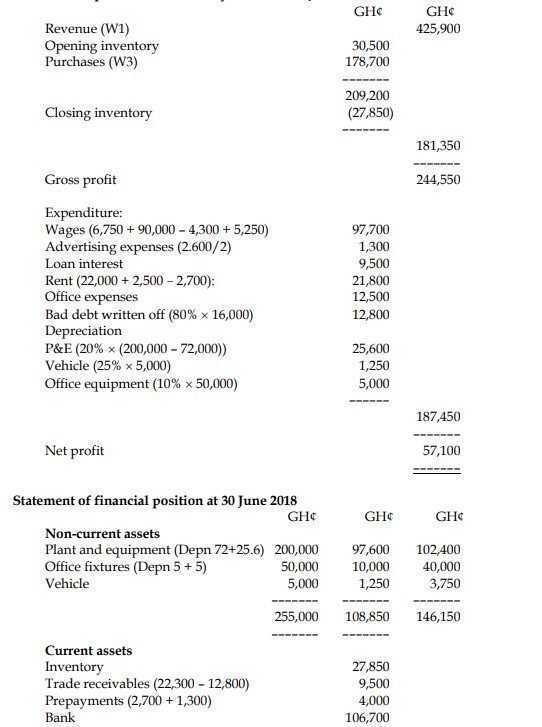

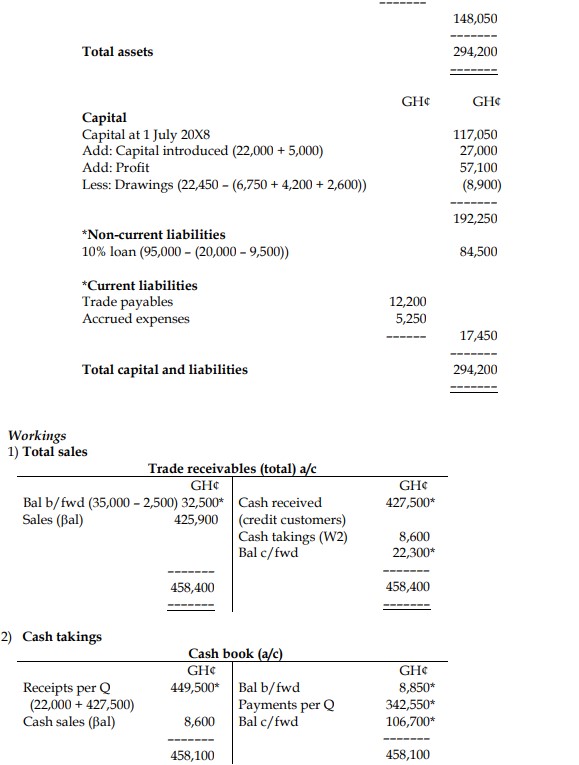

i) Inventory at 30 June 2019 was GH¢27,850.

ii) Depreciation is to be provided as follows:

- Plant and equipment 20% per annum, reducing balance basis

- Office equipment 10% per annum on cost

iii) During the year, Kofi introduced a motor vehicle valued at GH¢5,000 into the business. It is to be depreciated over 4 years on the straight-line basis with a full year’s depreciation charge in the year of acquisition.

iv) Prepayments and accrued expenses as at 30 June 2018 were: - Rent paid in advance GH¢2,500

- Accrued wages GH¢4,300

v) Cash drawings during the year included GH¢6,750 for wages, GH¢4,200 for cash payments to suppliers, and GH¢2,600 for advertising leaflets (of which half are yet to be distributed). The remainder was Kofi’s personal expenditure.

vi) The bank balance per the bank statement as at 30 June 2019 after adjusting for unpresented cheques was GH¢106,700. Any difference is assumed to be cash takings (i.e., in respect of cash sales).

vii) Loan repayments include interest amounting to GH¢9,500.

viii) At 30 June 2019 the following assets and liabilities existed: - Rent paid in advance GH¢2,700

- Accrued wages GH¢5,250

- Amounts due to suppliers GH¢12,200

- Amounts due from customers GH¢22,300

ix) On 3 July 2019, Kofi’s major customer, Yaw, went into liquidation owing GH¢16,000. A statement from the customer’s liquidator indicates that Kofi should expect to recover 20 pesewas for every GH¢1 owing.

Required:

Prepare Kofi’s statement of profit or loss for the year ended 30 June 2019 and a statement of financial position as at that date. Ignore taxation. (20 marks)

Answer

a) Statement of Profit or Loss for the year ended 30 June 2019

- Uploader: Theophilus