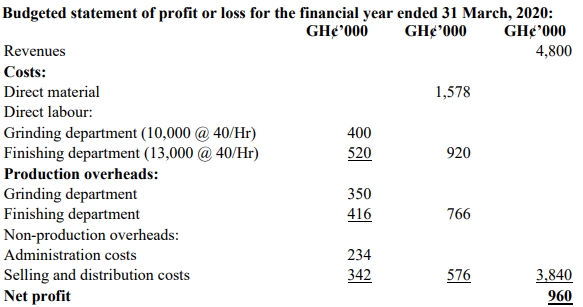

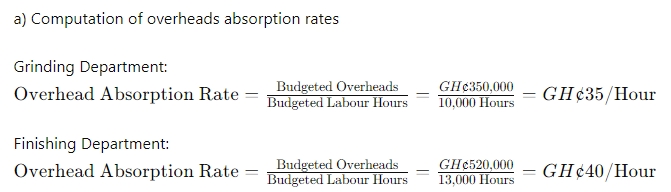

- 20 Marks

Question

a) Management accounting is the provision of financial and non-financial decision-making information to managers.

Required:

i) Explain the decision-making levels within an organization and state an example each of the kind of decision taken at the various levels. (9 marks)

ii) Explain TWO (2) sources of management accounting information and state an example each of the information to be obtained. (6 marks)

b) One form of specific order costing methods that seeks to attribute costs to jobs is known as job costing.

Required:

Enumerate THREE (3) factors that are necessary to ensure an effective and workable job costing system. (5 marks)

Answer

a)

i) Decision-Making Levels within an Organization:

- Strategic Level:

- Description: This level involves long-term decision-making that impacts the overall direction of the organization. Decisions are made by top management, including the board of directors and senior executives.

- Example: A decision to enter a new market or to discontinue a product line is made at this level.

- Tactical Level:

- Description: This level involves medium-term decisions that translate the strategies set at the strategic level into actionable plans. Middle management is typically responsible for these decisions.

- Example: A decision regarding the allocation of resources among different departments or projects to achieve the organization’s strategic goals is made at this level.

- Operational Level:

- Description: This level involves short-term decisions focused on the day-to-day operations of the organization. Operational decisions ensure that the organization runs efficiently on a daily basis.

- Example: A decision to reorder inventory or to schedule shifts for production workers is made at this level.

(3 points @ 3 marks each = 9 marks)

ii) Sources of Management Accounting Information:

- Internal Sources:

- Description: Information obtained from within the organization, including accounting records, production schedules, and human resource records.

- Example: Accounting records provide detailed information on costs, revenues, and profitability, which are used to monitor financial performance and make operational decisions.

- External Sources:

- Description: Information obtained from outside the organization, such as market research, industry reports, government publications, and competitor analysis.

- Example: Industry reports can provide benchmarking data that helps the organization assess its performance relative to competitors.

(2 points @ 3 marks each = 6 marks)

b) Factors Necessary for an Effective and Workable Job Costing System:

- Accurate Cost Allocation: A robust system must accurately allocate direct and indirect costs to specific jobs. This requires well-defined cost centers and an effective method for apportioning overheads.

- Detailed Documentation: Comprehensive documentation of all job-related costs, including materials, labor, and overheads, is essential to ensure accurate cost tracking and reporting.

- Timely and Accurate Data Entry: The system must ensure that all job-related data is entered promptly and accurately to provide real-time information for decision-making and cost control.

(3 points @ 1.67 marks each = 5 marks)

- Topic: Job Costing

- Series: MAR 2024

- Uploader: Joseph