Question

Answer

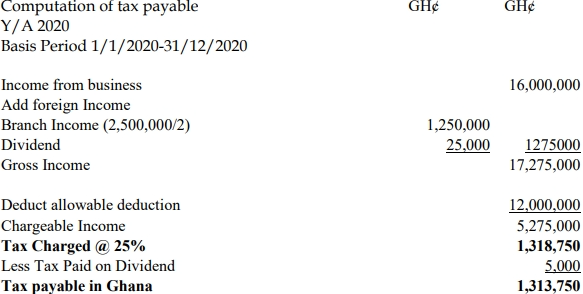

i) Computation of tax payable

Explanation:

Income received from a foreign country loses its character; hence, the dividend is added to the income, and the tax paid in the foreign country is given as credit. Additionally, the branch of the entity in Ghana has become a foreign PE, and therefore, its income for the first 183 days is taxable in Ghana. After that, it is exempt from tax.

ii) Computation of tax payable if the income from Zambia was earned in the last quarter of 2020

| Description | GH¢ | GH¢ |

|---|---|---|

| Income from business (Ghana) | 16,000,000 | |

| Add foreign income: | ||

| Dividend | 25,000 | |

| Gross Income | 16,025,000 | |

| Deduct allowable deduction | (12,000,000) | |

| Chargeable Income | 4,025,000 | |

| Tax Charged @ 25% | 1,006,250 | |

| Less tax paid on dividend | (5,000) | |

| Tax payable in Ghana | 1,001,250 |

Explanation:

Since the foreign Permanent Establishment did not earn the income in the first 183 days or first 6 months, the income shall be exempt from tax in Ghana in line with section 111 of Act 896 (Act 2015).