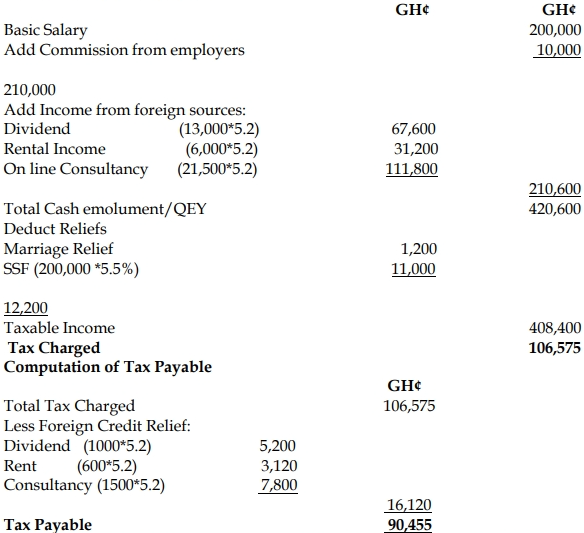

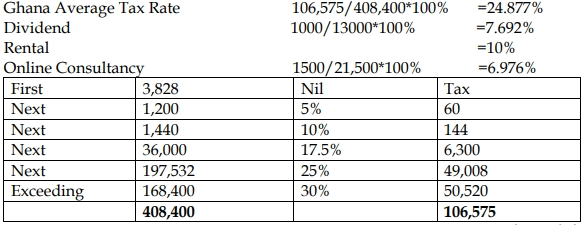

- 10 Marks

Question

The management of Smith Plc, a UK-based company, is considering the possibility of launching its presence in Ghana and it is not sure of the tax implication of the following under the tax laws of Ghana:

i) It is considering making its presence through incorporation in Ghana or creating an external company that is a Permanent Establishment (Branch) instead.

ii) It intends to acquire all its non-current assets through finance lease as against buying the assets outright when it makes its presence in Ghana.

iii) It intends to bring some staff from the United Kingdom to work in Ghana who will be paid half salary in Ghana and the other half paid directly to their accounts in the United Kingdom as against paying their full salary in Ghana.

iv) Management intends to acquire shares in many companies in Ghana as part of efforts to create value for shareholders through dividend receipts as against granting loans to interested companies in Ghana if it is unable to make its presence in Ghana.

Required:

Evaluate the above policy interventions and advise on the tax implication of each to enable the management of Smith Plc to make a decision.

Answer

i) Incorporation:

- A company incorporated in Ghana is required to pay a stamp duty of 0.5% on the value of shares introduced as stated capital and corporate taxes on profits. Additionally, dividends declared will be subject to an 8% withholding tax. PAYE deductions will be required for employees, with withholding taxes of 3%, 7.5%, or 5% applicable for various services, depending on whether the supplier is resident or non-resident (20% for non-residents).

Permanent Establishment (Branch): - A branch will pay corporate taxes on profits and an additional 8% branch profit tax. It will also follow PAYE and withholding tax rules as in the incorporation case, except that a branch is not liable to stamp duty.

- Conclusion: The tax implications for both options are similar except for the branch profit tax, which applies regardless of whether profits are repatriated, unlike dividends.

ii) Non-current assets acquired through finance lease:

- Capital allowance is granted on the capital portion of the lease rentals, while the interest portion is deductible if it meets tax deductibility criteria. For outright purchases, capital allowances apply on the acquisition amount.

iii) Payment of expatriates’ salaries:

- Income from Ghana is taxed based on the residence status of the employee. Paying part of the salary in Ghana and part abroad has no tax advantage since Ghana taxes the global income of residents.

iv) Acquisition of shares vs. granting loans:

- Dividends from shares acquired in Ghana are subject to an 8% withholding tax. Interest from loans granted will be subject to withholding tax of 8% for non-residents.

- Topic: International taxation, Permanent establishment

- Series: NOV 2018

- Uploader: Dotse