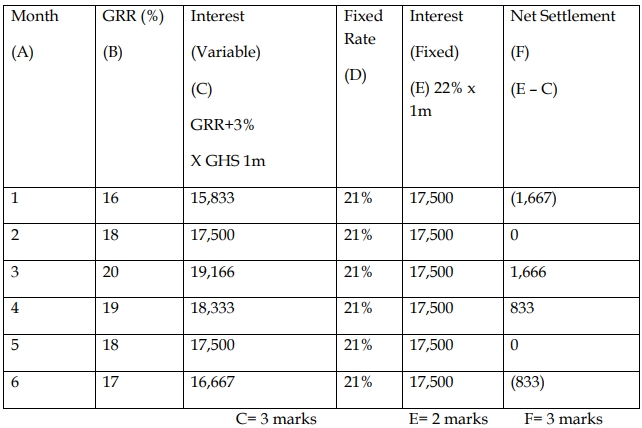

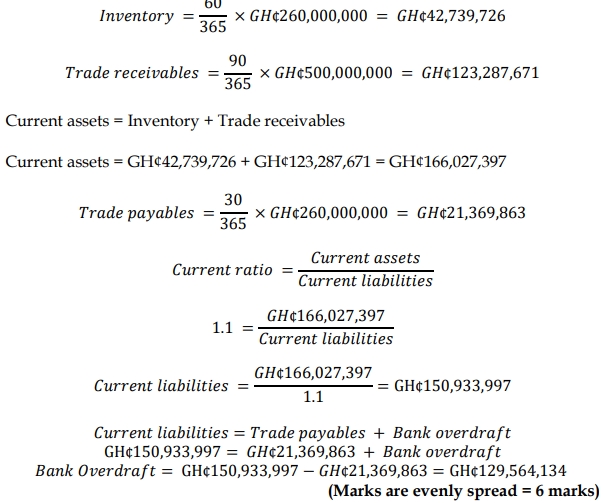

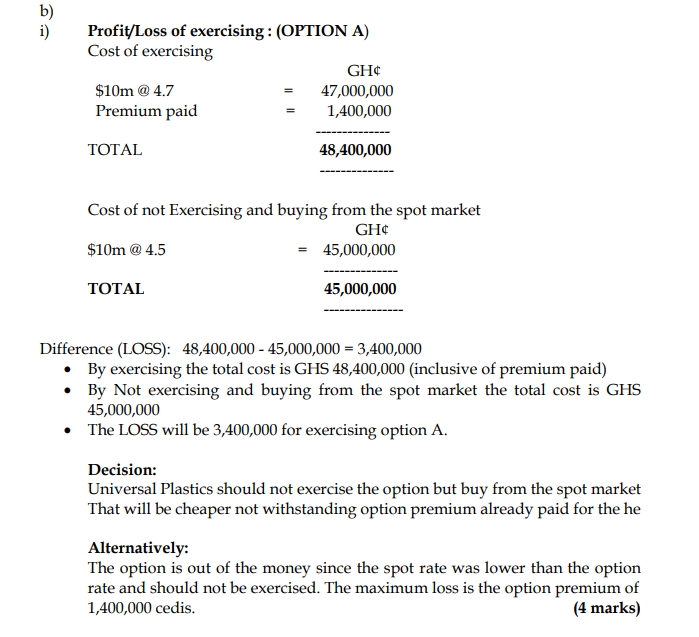

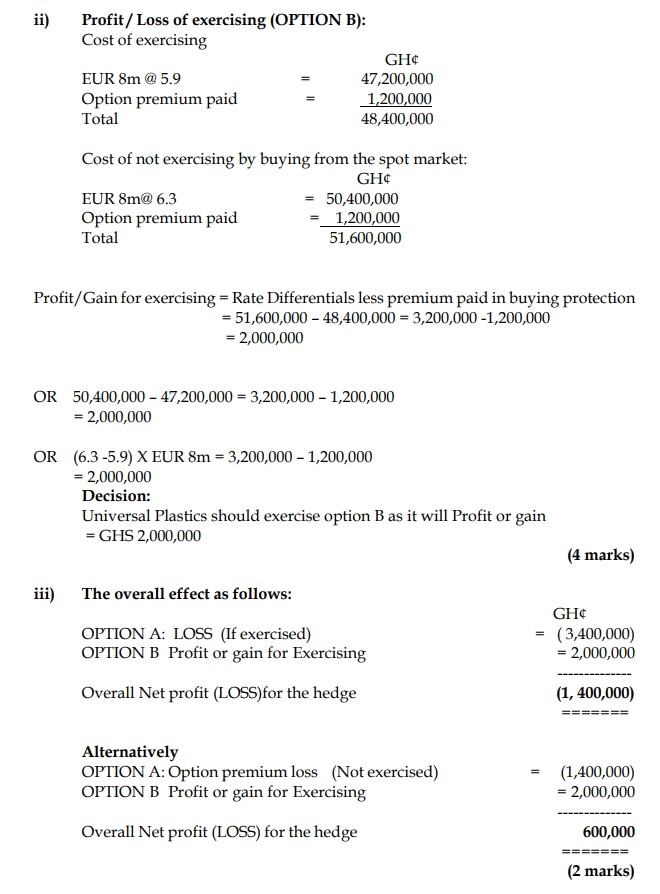

- 7 Marks

Question

i) Explain the term intrinsic value of an option. (1 mark)

ii) DUU Ghana Ltd bought USD/GH¢ call options from KASA Ltd. The table below shows the various spot rates and strike prices for the various tenors.

| Month | Spot Rate USD/GH¢ | Exercise Rate/Price USD/GH¢ |

|---|---|---|

| 1 | 5.1 | 4.8 |

| 2 | 5.3 | 5.0 |

| 3 | 5.5 | 5.4 |

| 4 | 5.8 | 5.8 |

| 5 | 5.7 | 6.0 |

| 6 | 6.0 | 6.4 |

Required:

Determine the intrinsic value of the option for each trading month and clearly indicate the months in which the option is in-the-money, at-the-money, or out-of-the-money. (6 marks)

Answer

i) Intrinsic value of an option:

The intrinsic value of an option is the amount by which the option is in-the-money. It is the positive value or gain that would be realized if the option were exercised immediately. An option has intrinsic value when it is in-the-money, meaning that for a call option, the spot price is above the exercise price.

(1 mark)

ii) Intrinsic value calculation:

| Month | Spot Rate USD/GH¢ | Exercise Rate USD/GH¢ | Intrinsic Value (Spot Rate – Exercise Rate) | Comments/Interpretation |

|---|---|---|---|---|

| 1 | 5.1 | 4.8 | 0.3 | In-the-money |

| 2 | 5.3 | 5.0 | 0.3 | In-the-money |

| 3 | 5.5 | 5.4 | 0.1 | In-the-money |

| 4 | 5.8 | 5.8 | 0 | At-the-money |

| 5 | 5.7 | 6.0 | (0.3) | Out-of-the-money |

| 6 | 6.0 | 6.4 | (0.4) | Out-of-the-money |

Interpretation:

- DUU Ltd was in-the-money for months 1, 2, and 3.

- The option was at-the-money in month 4.

- The option was out-of-the-money in months 5 and 6.

- Tags: Currency risk, Hedging, Intrinsic value, Options

- Level: Level 2

- Topic: Futures and hedging with futures, Hedging with options

- Series: NOV 2020

- Uploader: Theophilus