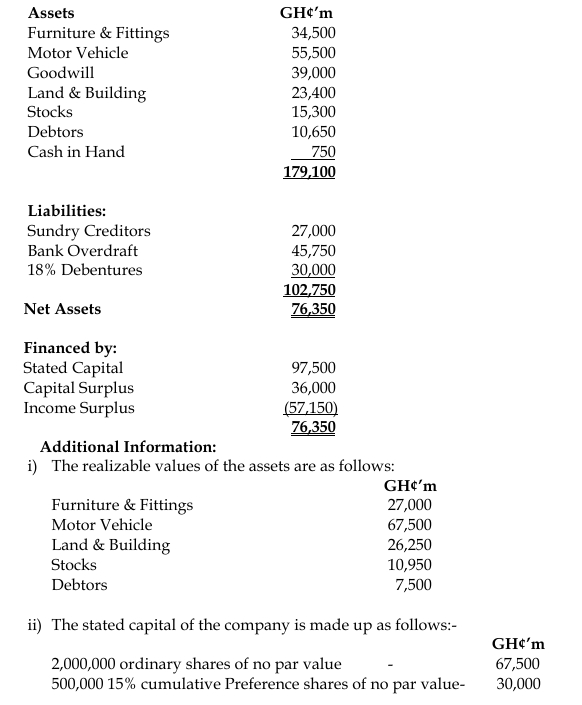

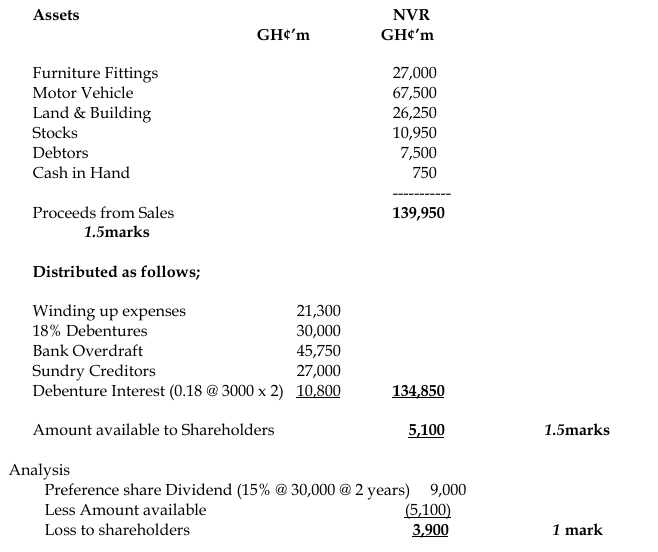

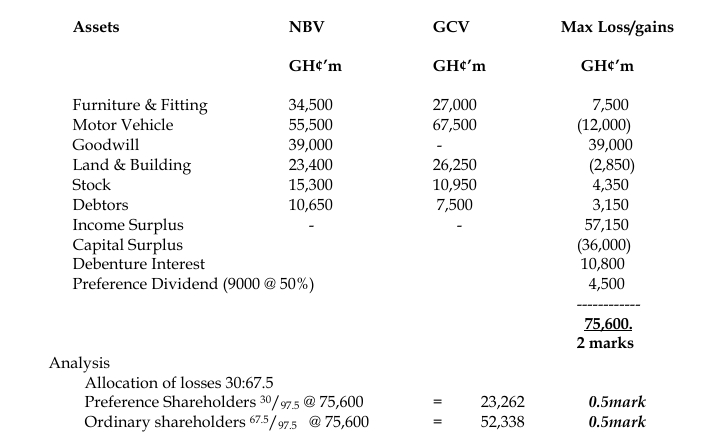

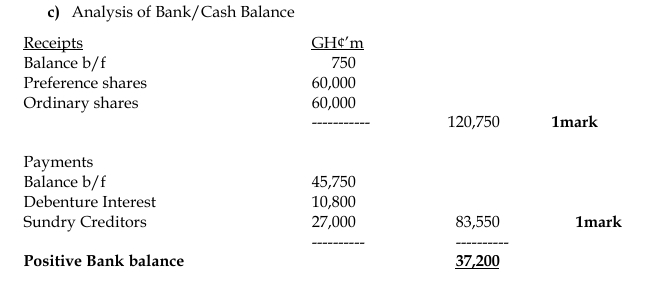

- 10 Marks

Question

There are many possible reasons why management would wish to restructure a company’s finances. A reconstruction scheme might be agreed upon when a company is in danger of being put into liquidation.

Required:

i) Distinguish between a leveraged buy-out and leveraged recapitalisation. (4 marks)

ii) What are the THREE main types of reconstruction? Describe them briefly. (3 marks)

iii) Describe the procedures that should be followed when designing a financial reconstruction scheme. (3 marks)

Answer

i) Difference Between Leveraged Buy-out and Leveraged Recapitalisation:

- Leveraged Buy-out (LBO):

A leveraged buy-out occurs when a group of investors uses a significant amount of borrowed money (leverage) to acquire a company. The assets of the company being acquired, along with the acquiring company’s assets, are often used as collateral for the loans. LBOs are typically used to take over large companies without having to commit significant capital upfront. - Leveraged Recapitalisation:

Leveraged recapitalisation is a strategy used by a company to increase its debt levels in order to pay a large dividend to shareholders or buy back shares. Unlike an LBO, a leveraged recapitalisation does not involve the acquisition of another company but is rather focused on altering the company’s capital structure to return value to its existing shareholders.

(4 marks)

ii) The Three Main Types of Reconstruction:

- Financial Reconstruction:

This type of reconstruction involves altering the company’s capital structure, which may include issuing new shares, renegotiating debt, or converting debt into equity. - Portfolio Reconstruction:

This involves changing the company’s assets by either acquiring new businesses or divesting existing ones, such as through acquisitions or spin-offs. - Organizational Reconstruction:

This entails restructuring the company’s management or operational structure, which could involve layoffs, merging departments, or a complete overhaul of the company’s leadership or divisions.

(3 points for 3 marks)

iii) Procedures for Designing a Financial Reconstruction Scheme:

- Estimate the Position of Each Party:

The first step is to evaluate the financial position of all stakeholders (creditors, shareholders, etc.) if liquidation were to occur. This establishes the minimum acceptable outcome for each group. - Assess Additional Sources of Finance:

The next step is to explore other funding options, such as selling off non-core assets, issuing new shares, or raising additional loans. This can provide the necessary capital to keep the company afloat. - Design a Capital Restructure Scheme:

A new capital structure must be devised that satisfies all parties involved. This may involve renegotiating debt terms, issuing new equity, or adjusting the ownership structure. - Evaluate the Post-Reconstruction Position:

The company’s financial viability must be assessed after reconstruction, ensuring that it can operate sustainably with the new structure.

(3 marks)

- Topic: Business reorganisation, Financial reconstruction

- Series: MAY 2017

- Uploader: Dotse