- 1 Marks

Question

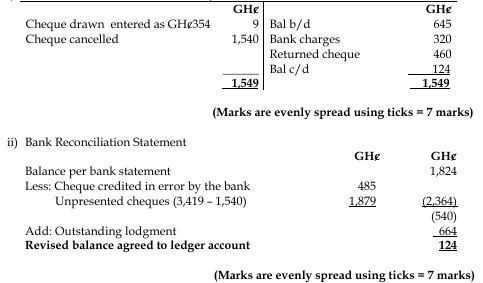

The bank column in the cash book shows a credit balance of N50,000. This means:

A. A total payment of N50,000

B. A gross receipt of N50,000

C. A balance of N50,000 in the bank

D. An overdraft of N50,000

E. A balance of N50,000 cash

Answer

Answer:

D. An overdraft of N50,000

Explanation:

A credit balance in the bank column of the cash book signifies that the business has an overdraft. This means that the business has spent more money than is available in the bank account, resulting in a negative or overdraft balance. The bank account is overdrawn by N50,000.

- Tags: Bank Balance, Cash Book, Overdraft

- Level: Level 1

- Topic: Bank reconciliations

- Series: MAY 2016

- Uploader: Joseph