Question

Answer

a) Strengths and Weaknesses of FVL (6 marks)

Strengths:

- The schoolmate’s hands-on experience coupled with Peter’s competence in drawing and designing are complementary and indispensable to gaining a competitive advantage. They are highly skilled, ambitious, and have a passion for the job. Peter believes the company should continue to exclusively rely on the engagement of experienced hands from the industry.

- The small size of the workforce allows them to fully dedicate themselves to their tasks to produce high-quality products.

- Few competitors in the Ghanaian luxury shoemaking industry. The footwear-making industry in Ghana has an influx of local artisans mainly from Kumasi who produce semi and low-quality shoes at very low prices compared to FVL. They therefore do not pose much threat to FVL, taking into consideration the target market of affluent and well-off customers who are willing to spend more than most.

- FVL has a strong tertiary presence compared to its competitors in Ghana. They do direct sales to students on campuses, and this also helps the company to promote its brand.

Weaknesses:

- The raw materials used to produce FVL’s products are sourced from abroad due to unavailability of such quality in the country. This serves as extra cost for the company due to import, handling, and shipping charges plus extra charge from local importers.

- Inadequate funding and lack of access to funding from financial institutions due to lack of credit history.

- Inadequate resources to open its own sales outlets as the shoes produced are largely distributed through major retail shops dotted across the country. This could result in price differentials among the various retail shops.

- Not a strong brand internationally as compared to international competitors. The brand is not well known amongst the affluent masses in foreign countries as its advertisement does not reach those boundaries.

b) Report on the Process of Strategic Management (8 marks)

Introduction:

The strategic management process means defining the organization’s strategy. It is also defined as the process by which managers make a choice of a set of strategies for the organization that will enable it to achieve better performance.

Strategic management is a continuous process that appraises the business and industries in which the organization is involved; appraises its competitors; and fixes goals to meet all the present and future competitors and then reassesses each strategy.

Strategic Management Process:

- Environmental Scanning: Environmental scanning refers to a process of collecting, scrutinizing, and providing information for strategic purposes. It helps in analyzing the internal and external factors influencing an organization. After executing the environmental analysis process, management should evaluate it on a continuous basis and strive to improve it.

- Strategy Formulation: Strategy formulation is the process of deciding the best course of action for accomplishing organizational objectives and hence achieving organizational purpose. After conducting environmental scanning, managers formulate corporate, business, and functional strategies.

- Strategy Implementation: Strategy implementation implies making the strategy work as intended or putting the organization’s chosen strategy into action. Strategy implementation includes designing the organization’s structure, distributing resources, developing decision-making processes, and managing human resources.

- Strategy Evaluation: Strategy evaluation is the final step of the strategy management process. The key strategy evaluation activities are: appraising internal and external factors that are the root of present strategies, measuring performance, and taking remedial/corrective actions. Evaluation ensures that the organizational strategy, as well as its implementation, meets the organizational objectives.

Conclusion:

These components are steps that are carried out in chronological order when creating a new strategic management plan. FVL, which is in the process of institutionalizing a strategic approach, will revert to these steps as per the situation’s requirements, so as to make essential changes.

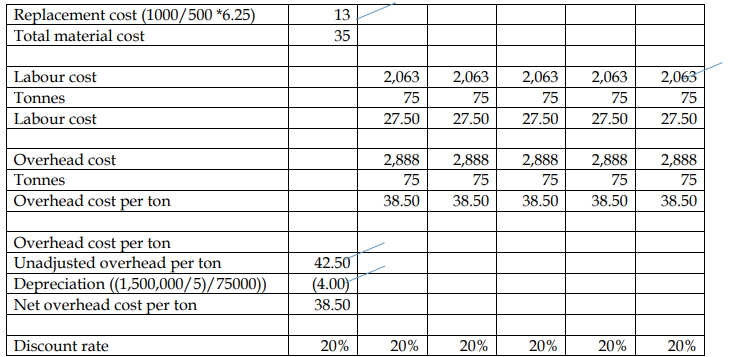

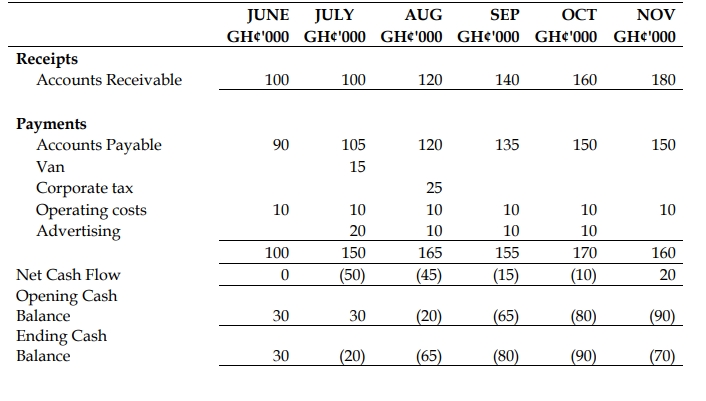

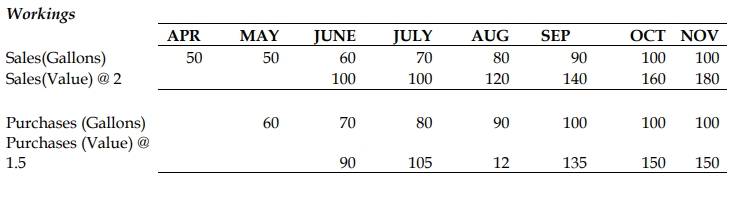

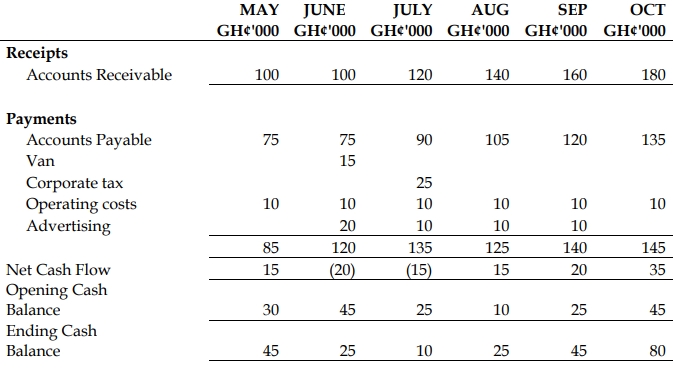

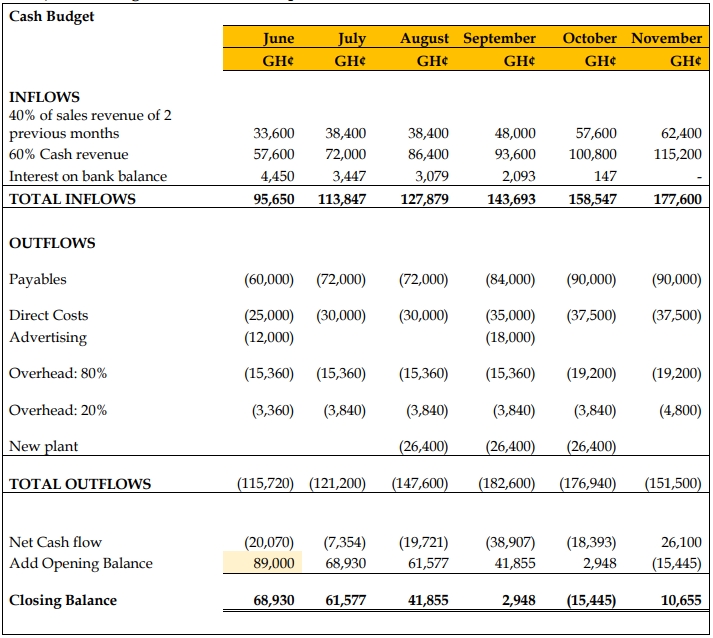

c) Cash Budget for the Six-Month Period (12 marks)

d) Strategies for Overcoming the Liquidity Crisis of FVL (8 marks)

- Directing FVL’s accounts receivable department to bill its customers in a timely fashion and chase any unpaid invoices as soon as they become past due. Money tied up in unpaid invoices can cause FVL serious liquidity problems. The Directors should consider offering its customers a discount for settling their bills early.

- Analyzing FVL’s overhead and looking for cost savings. Studying all areas of FVL’s business to see where they can save money and free up funds to bolster its liquidity.

- Selling off inventory and assets that are tying up FVL’s cash. Stock that’s been sitting in FVL’s storeroom for six months is costing the firm money. Discount any inventory that’s proving hard to shift to get cash flowing back into FVL business. Sell assets it rarely uses.

- Discussing short-term funding options with FVL’s bank or other lenders. FVL’s bank might be willing to extend FVL’s credit line to help it overcome liquidity problems. If FVL’s bank is unable to help, approach other lenders or sell some of the equity in FVL to an investor to overcome cash flow problems.

- Negotiating new terms with FVL’s suppliers. Ask for a longer period to settle invoices or discuss the possibility of taking stock on a sale-or-return basis. If FVL has been a good customer in the past, there’s a good chance it can come to an arrangement, especially if any new deal boosts the amount of goods or services it is able to buy.

e) Methods for Raising Long-Term Capital (6 marks)

- Issue of Shares: Involves the public issue of equity and preference shares in the Ghana stock exchange. Issuing shares is the most common method of raising long-term capital because there are various investors who are ready to invest in the capital market. Therefore, shares are used to finance projects having long gestation periods.

- Issue of Debentures: Involves the collection of funds by issuing debentures. When FVL issues debentures, it needs to pay a fixed rate of interest to debenture holders.

- Term Loans: Refers to the funds that are raised from financial institutions for financing long-term projects. The rate of interest on term loans is higher than the rate of interest on debentures.

- Fund from Operations: Refers to the fund raised by FVL’s own operations. It is the accumulated profit of FVL and can be used to finance various short-term and long-term projects.

- Sale of Fixed Assets: Helps in generating funds by selling fixed assets, such as land, buildings, plants, and machinery to finance short-term and long-term projects. However, the usage of this method may hamper the goodwill and creditworthiness of FVL.

|

|