Question

Answer

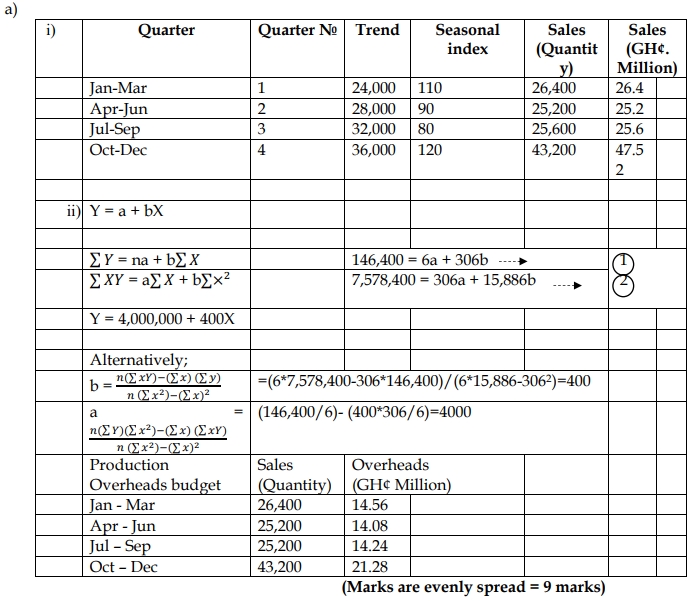

b.) Seasonal adjustment separates a time series into trend-cycle, seasonal, and

irregular components.

i) Trend-Cycle (C):

This component represents the long-term movement or pattern in a time series, which is typically derived from surrounding years or periods of observations. It shows the underlying direction in which the data is moving, whether upward, downward, or stagnant, over an extended period. (2 marks)

ii) Seasonal Components (S):

Seasonal components are regular, predictable fluctuations that occur within specific periods such as months or quarters. These effects are stable in timing, direction, and magnitude and can be caused by factors like weather patterns, holidays, or other recurring events. (2 marks)

iii) Irregular Components (I):

Irregular components are unpredictable fluctuations in a time series that cannot be attributed to trend or seasonal effects. They are usually short-term, random variations caused by unforeseen events such as natural disasters, strikes, or economic shocks. (2 marks)

c) Activities Involved in Providing Information for Control Purposes:

- Monitoring Actual Performance: This involves tracking and measuring actual outcomes against planned or budgeted objectives to assess performance.

- Evaluating Actual Performance: This step involves analyzing the data to determine how well the organization has met its goals and identifying areas of improvement.

- Taking Control Action: If there are deviations from the plan, corrective actions are taken to bring performance back in line with objectives. This may involve adjusting processes, reallocating resources, or revising targets.

(3 points @ 1.667 marks each = 5 marks)