- 20 Marks

Question

Obiya Ltd assembles computer equipment from bought-in components and distributes them to various wholesalers and retailers. It has recently subscribed to an inter-firm comparison service. Members submit accounting ratios as specified by the operator of the service, and in return, members receive the average figures for each of the specified ratios taken from all of the companies in the same sector that subscribe to the service. The specified ratios and the average figures for Obiya’s sector are shown below:

Ratios of sector companies for the period to 30 September 2017

| Ratio | Sector Average |

|---|---|

| Return on capital employed | 22.1% |

| Net asset turnover | 1.8 times |

| Gross profit margin | 30% |

| Net profit (before tax) margin | 12.50% |

| Current ratio | 1.6:1 |

| Quick ratio | 0.9:1 |

| Inventory holding period | 46 days |

| Accounts receivable collection period | 45 days |

| Accounts payable payment period | 55 days |

| Debt to equity | 40% |

| Dividend yield | 6% |

| Dividend cover | 3 times |

Obiya Ltd’s financial statements for the year to 30 September 2017 are set out below:

Statement of profit or loss for the year ended 30 September 2017

| Description | GH¢’000 |

|---|---|

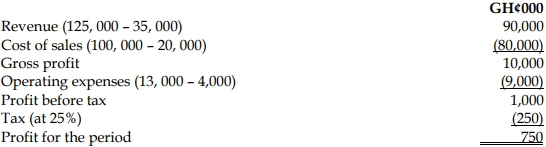

| Revenue | 2,425 |

| Cost of sales | (1,870) |

| Gross profit | 555 |

| Other operating expenses | (215) |

| Operating profit | 340 |

| Finance costs | (34) |

| Exceptional item (note ii) | (120) |

| Profit before tax | 186 |

| Income tax | (90) |

| Profit for the period | 96 |

Statement of changes in equity (extract)

For the year ended 30 September 2017

| Description | GH¢’000 |

|---|---|

| Retained earnings – 1 October 2016 | 179 |

| Net profit for the period | 96 |

| Dividends paid (Interim GH¢60,000; final GH¢30,000) | (90) |

| Retained earnings – 30 September 2017 | 185 |

Statement of financial position as at 30 September 2017

| Description | GH¢’000 |

|---|---|

| Non-current assets | |

| Property, plant, equipment | 540 |

| Current assets | |

| Inventory | 275 |

| Accounts receivable | 320 |

| Bank | – |

| Total current assets | 595 |

| Total assets | 1,135 |

| Equity | |

| Ordinary shares (25 pesewas each) | 150 |

| Retained earnings | 185 |

| Total equity | 335 |

| Non-current liabilities | |

| 8% loan notes | 300 |

| Current liabilities | |

| Bank overdraft | 65 |

| Trade accounts payable | 350 |

| Taxation | 85 |

| Total current liabilities | 500 |

| Total equity and liabilities | 1,135 |

Notes:

i) The details of the non-current assets are:

| Description | Cost (GH¢’000) | Accumulated depreciation (GH¢’000) | Net book value (GH¢’000) |

|---|---|---|---|

| At 30 September 2017 | 3,600 | 3,060 | 540 |

ii) The exceptional item relates to losses on the sale of a batch of computers that had become worthless due to improvements in microchip design.

iii) The market price of Obiya’s shares throughout the year averaged GH¢6.00 each.

Required:

a) Calculate the ratios for Obiya equivalent to those provided by the inter-firm comparison service.

(5 marks)

b) Write a report analyzing the operational performance, gearing, investment, and liquidity of Obiya Ltd based on a comparison with the sector averages. (10 marks)

Answer

Ratios for Obiya Ltd for the period to 30 September 2017:

| Description | Obiya Ltd |

|---|---|

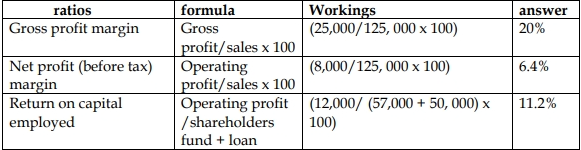

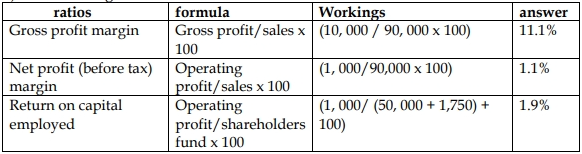

| Return on capital employed (186 + 34 loan interest ÷ (335 + 300)) | 34.6% |

| Net asset turnover (2,425 ÷ (335 + 300)) | 3.8 times |

| Gross profit margin (555 ÷ 2,425 × 100) | 22.9% |

| Net profit margin (186 ÷ 2,425 × 100) | 7.7% |

| Current ratio (595 ÷ 500) | 1.19:1 |

| Quick ratio (320 ÷ 500) | 0.64:1 |

| Inventory holding period (275 ÷ 1,870 × 365) | 54 days |

| Accounts receivable collection period (320 ÷ 2,425 × 365) | 48 days |

| Accounts payable payment period (350 ÷ 1,870 × 365) | 68 days |

| Debt to equity (300 ÷ 335 × 100) | 90% |

| Dividend yield (15p ÷ GH¢6 × 100) | 2.5% |

| Dividend cover (96 ÷ 90) | 1.07 times |

(5 marks evenly spread)

b)

Report on Financial Performance of Obiya Ltd

To: Management of Obiya Ltd

From: Financial Analyst

Subject: Analysis of Financial Performance, Gearing, Investment, and Liquidity Compared to Sector Averages

1. Operational Performance:

- Return on Capital Employed (ROCE):

Obiya’s ROCE of 34.6% is significantly higher than the sector average of 22.1%. This indicates that Obiya is more efficient in generating profits from its capital employed. The high ROCE is largely driven by a higher Net Asset Turnover of 3.8 times compared to the sector’s 1.8 times. However, this high turnover may be partly due to the relatively old and fully depreciated non-current assets, which could require replacement soon. - Gross Profit Margin:

Obiya’s gross profit margin of 22.9% is lower than the sector average of 30%. This suggests that Obiya may be facing higher cost pressures or competitive pricing challenges. - Net Profit Margin:

The net profit margin of 7.7% is also below the sector average of 12.5%. The impact of the exceptional item (GH¢120,000 loss on inventory) worsens the profit margin, indicating potential issues with inventory management and technological obsolescence. Excluding this, Obiya’s profitability would improve but still remain below the sector.

2. Liquidity:

- Current Ratio:

Obiya’s current ratio of 1.19:1 is below the sector average of 1.6:1, indicating that the company may struggle to cover its short-term liabilities. - Quick Ratio:

The quick ratio of 0.64:1 is also lower than the sector average of 0.9:1, highlighting liquidity challenges, especially if inventory becomes difficult to liquidate quickly. - Accounts Payable and Receivable:

Obiya’s accounts payable payment period is 68 days, significantly higher than the sector average of 55 days, which may suggest that Obiya is taking longer to pay its suppliers. This could damage supplier relationships. The accounts receivable collection period is 48 days, which is close to the sector average of 45 days.

3. Gearing:

- Debt to Equity:

Obiya’s debt to equity ratio of 90% is more than double the sector average of 40%. The company is highly leveraged, which poses financial risk, especially given its lower liquidity ratios. Although the company benefits from low-interest payments (8%), the high gearing could become problematic if profitability declines further or if it struggles to meet debt obligations.

4. Investment:

- Dividend Yield and Cover:

Obiya’s dividend yield of 2.5% is considerably lower than the sector average of 6%. Additionally, the dividend cover of 1.07 times (compared to the sector’s 3 times) indicates that almost all the company’s earnings are being paid out as dividends, leaving little room for reinvestment or to cushion against financial difficulties. This might not be sustainable in the long run.

Conclusion:

While Obiya Ltd demonstrates strong operational efficiency in terms of asset turnover, its profitability margins are weaker compared to the sector, and it faces significant liquidity and gearing challenges. Additionally, its investment return for shareholders is below sector expectations, and the company’s dividend policy appears unsustainable. Immediate attention should be given to improving liquidity, addressing high debt levels, and managing inventory more effectively to avoid future losses.

(10 marks evenly spread)

- Tags: Financial Performance, Gearing, Investment, Liquidity, Profitability, Ratio Analysis

- Level: Level 2

- Topic: Financial Statement Analysis

- Series: MAY 2018

- Uploader: Dotse