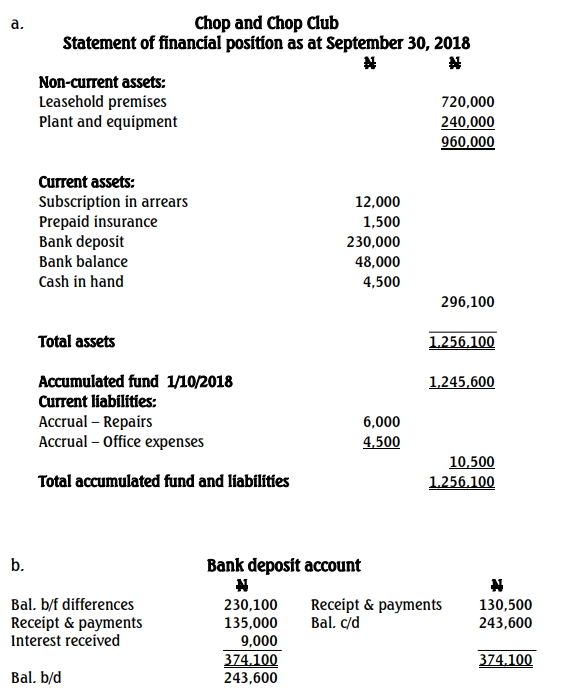

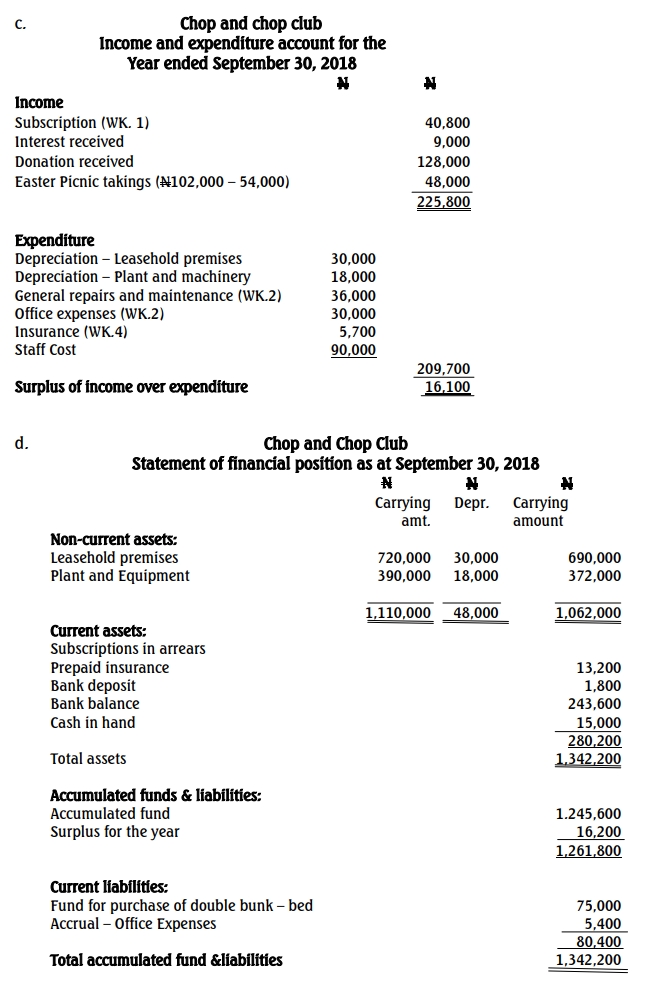

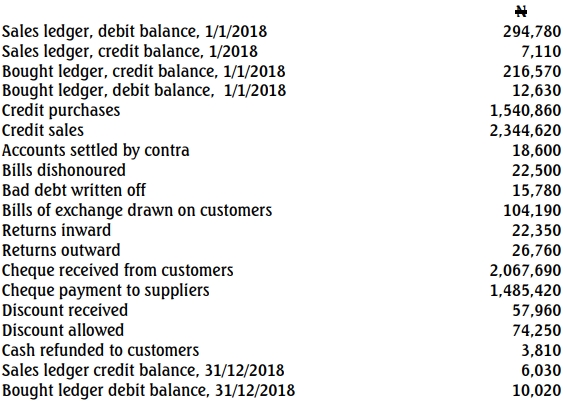

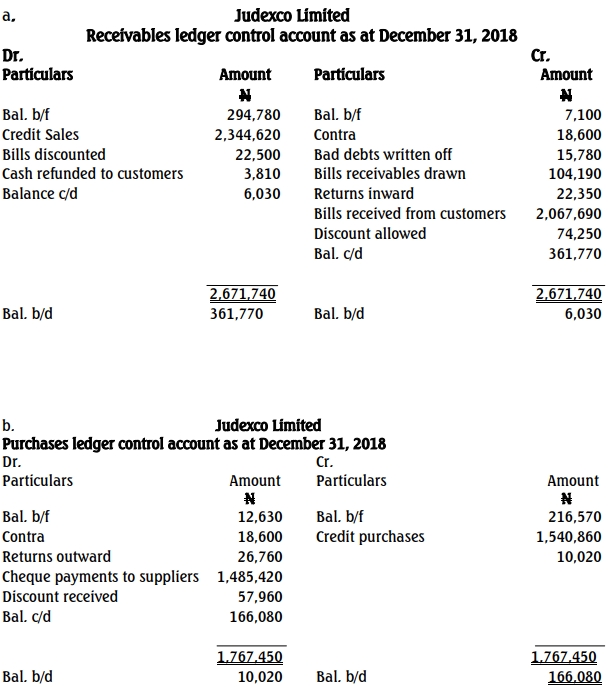

Question

Babatunde and Rasheed have been in partnership for several years, sharing profits and losses in the ratio 2:1 respectively. Their statement of financial position as at December 31, 2019, is shown below:

Required:

Prepare the following accounts:

a. Revaluation account

b. Capital accounts

c. Bank account

Answer