Question

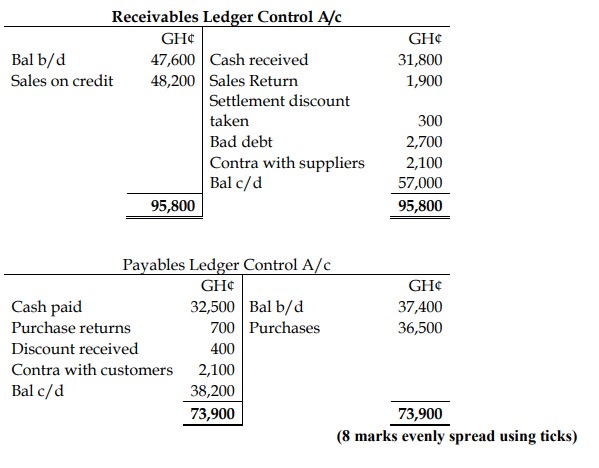

a) At the close of business on 31 July 2019, the following balances were extracted from the books of Kwabena Ltd, a limited liability company:

| Account | Amount (GH¢) |

|---|---|

| Receivables ledger control account | 47,600 |

| Payables ledger control account | 37,400 |

During the month of August, the following transactions occurred:

| Transaction | Amount (GH¢) |

|---|---|

| Cash received from customers | 31,800 |

| Cash paid to suppliers | 32,500 |

| Sales on credit | 48,200 |

| Purchases on credit | 36,500 |

| Sales returns | 1,900 |

| Purchase returns | 700 |

| Discounts received from suppliers | 400 |

| Settlement discount claimed by customer | 300 |

| Bad debts written off | 2,700 |

| Customer and supplier accounts settled by contra | 2,100 |

Required:

Prepare the receivables ledger control account and payables ledger control account for the month of August 2019 and hence determine the balances as at 31 August 2019.

(8 marks)

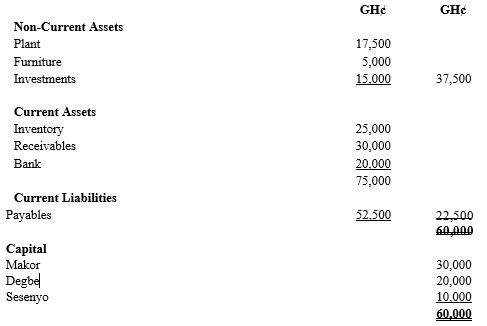

b) Makor, Degbe, and Sesenyo were in partnership sharing profits one-half, one-third, and one-sixth respectively. On 1 January 2019, they admitted Asinyo into the partnership on the following terms:

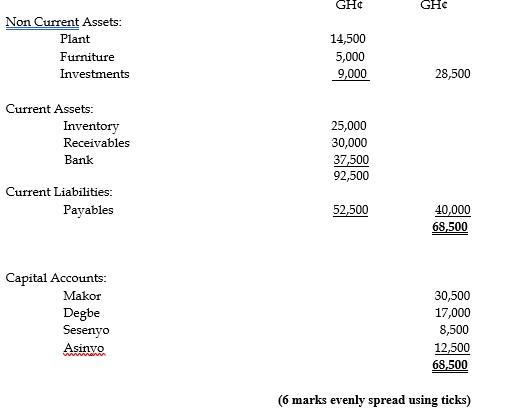

- Asinyo to have one-sixth share which he purchased from Makor, paying her GH¢20,000 for that share of goodwill. Of this amount, Makor retained GH¢15,000 and put the balance into the firm as additional capital. Asinyo also brought GH¢12,500 capital into the firm.

- It was agreed that the investments should be reduced to their market value of GH¢9,000 and that the plant should be reduced to GH¢14,500 as at 31 December 2018.

The Statement of Financial Position of the old firm as at 31 December 2018 was as follows:

Required:

i) Prepare the opening statement of financial position of the new firm as at 1 January 2019.

(6 marks)

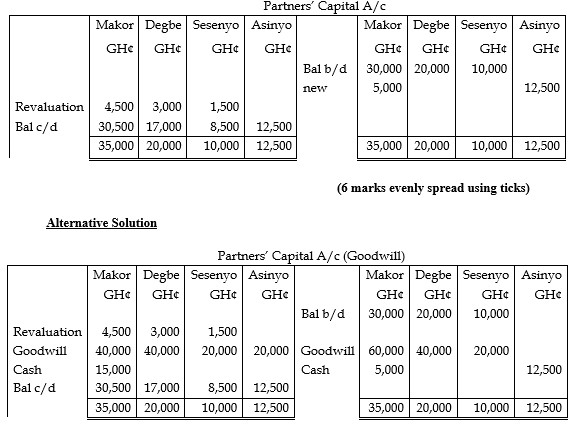

ii) Prepare the capital accounts of the partners for the year to 31 December 2019.

(6 marks)

Answer

a) Receivables Ledger Control Account

b) i) Opening Statement of Financial Position as at 1 January 2019

ii) Partners’ Capital Account for the year ended 31 December 2019

Workings

- Total value of goodwill 1/6 =20,000, Total goodwill = 20,000×6=120,000

- Makor ½ x 120,000 = 60,000.

- Degbe 1/3 x 120,000 = 40,000.

Sesenyo 1/6 x 120,000 = 20,000

- Calculation of the new ratio: Makor’s share = 1/2-1/6=1/3

Therefore, new ratio is 1/3 :1/3:1/6:1/6 =2 :2: 1:1