Question

Answer

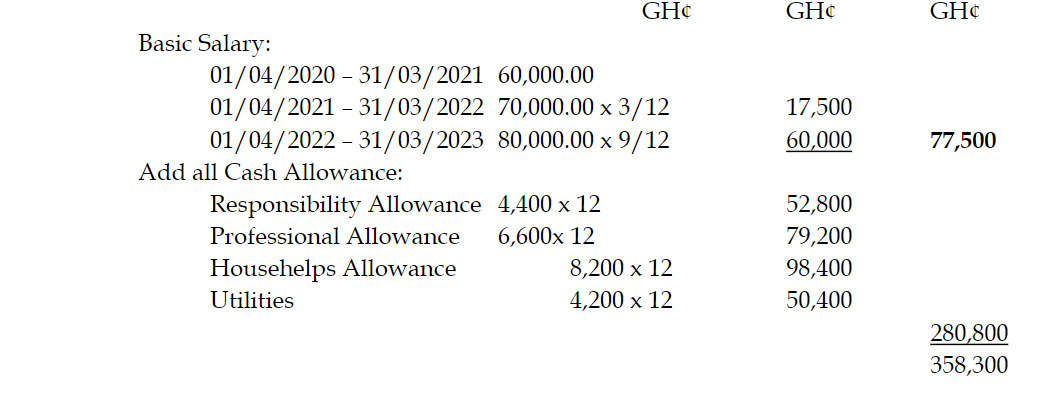

Antitom Computation Of Chargeable Income Year Of Assessment: 2022

Basis Period: January to December, 2022

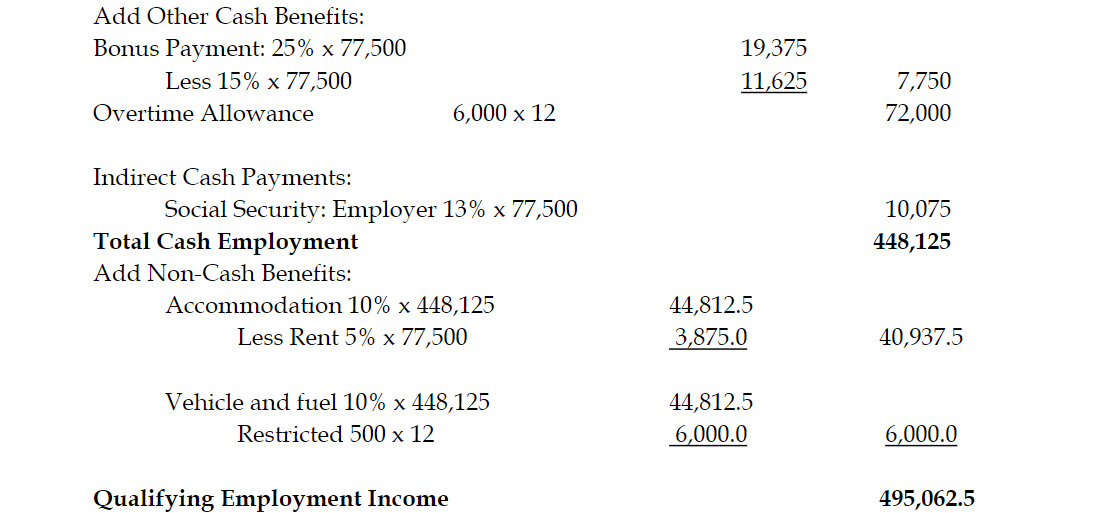

Add Other Cash Benefits:

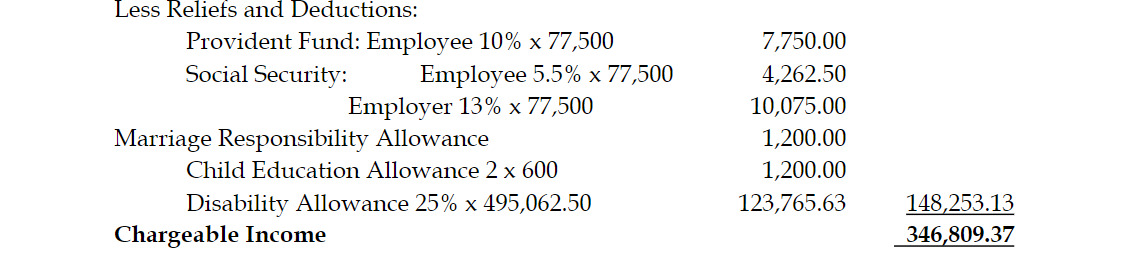

Less Reliefs and Deductions:

Note: Candidates who considered the non-taxation of interest and dividend income correctly were awarded marks.

(20 marks evenly spread using ticks)