- 20 Marks

Question

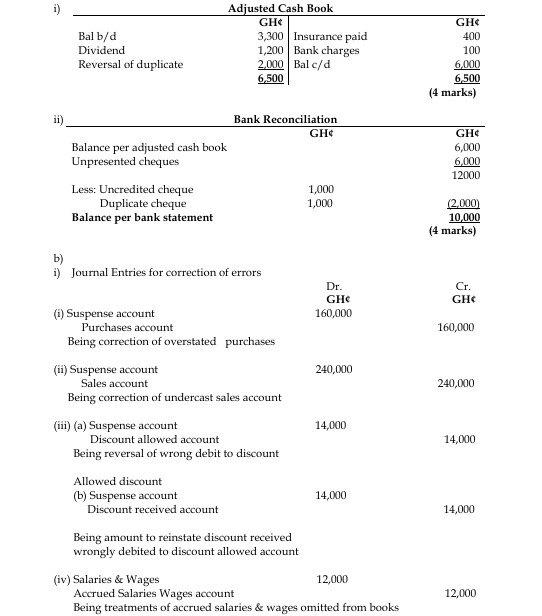

a) Markson’s & Co.’s cash book balance and bank statement balance at 31 March 2021 do not agree. The following information has been provided to help reconcile the difference:

- The balance per the bank statement is GH¢10,000 while that of the cash book is GH¢3,300.

- A cheque of GH¢6,000 issued to a supplier on 30 March 2021 was still in the supplier’s possession.

- Insurance paid by the bank is GH¢400. This is yet to be recorded in the cash book.

- An outgoing cheque of GH¢2,000 was recorded twice in the cash book. It is accurately recorded in the bank statement.

- Payment of a GH¢1,000 cheque is recorded twice in the bank statement.

- The bank statement recorded an amount of GH¢1,200 as dividends received from Kankam Ltd. There is no such transaction in the cash book.

- A cheque of GH¢1,000 received from a customer was deposited at the bank on 29 March 2021, but this amount has not yet reflected in the bank statement.

- Bank charges in the bank statement amounted to GH¢100.

Required:

i) Prepare an adjusted cash book to record transactions omitted. (4 marks)

ii) Prepare a bank reconciliation statement to agree the bank statement balance with the balance arrived at in (i) above. (4 marks)

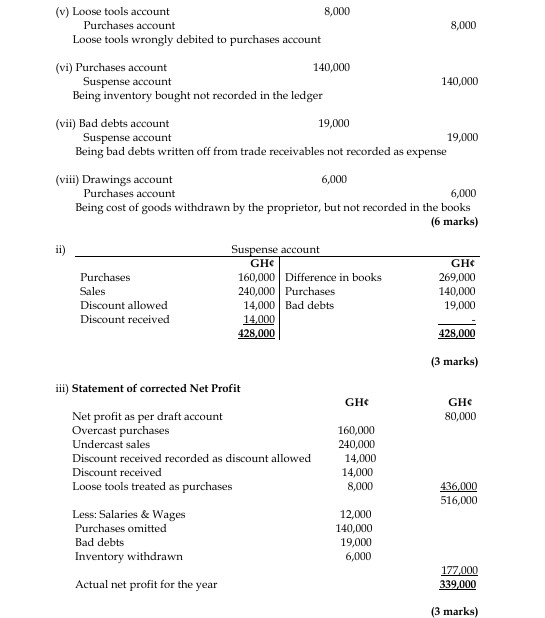

b) The trial balance of Askat Enterprises as at 31 December 2021 failed to agree. A suspense account was opened for the difference. Draft final accounts were prepared that revealed a net profit of GH¢80,000 for the year ended 31 December 2021. The following errors were subsequently discovered:

- The purchases day book total of GH¢160,000 had been posted to the ledger as GH¢320,000.

- The sales account has been understated by GH¢240,000.

- Discounts received of GH¢14,000 had been debited to discounts allowed account.

- An accrued salary and wages of GH¢12,000 was omitted.

- Loose tools bought for GH¢8,000 had been debited to the purchases account.

- Purchases of inventory for GH¢140,000 had not been posted to the ledger.

- Bad debts of GH¢19,000 written off in the trade receivables account had not been treated in the expense account.

- The proprietor had withdrawn goods worth GH¢6,000 for personal use. No entries had been made in the books.

Required:

i) Prepare the journal entries to correct the errors. (6 marks)

ii) Prepare the suspense account and show the difference in the books. (3 marks)

iii) Prepare a statement to show the correct net profit for the year. (3 marks)

Answer

- Tags: Bank Reconciliation, Cash Book, Error Correction, Suspense account

- Level: Level 1

- Topic: Bank reconciliations, Correction of errors

- Series: MAR 2023

- Uploader: Theophilus