Question

Answer

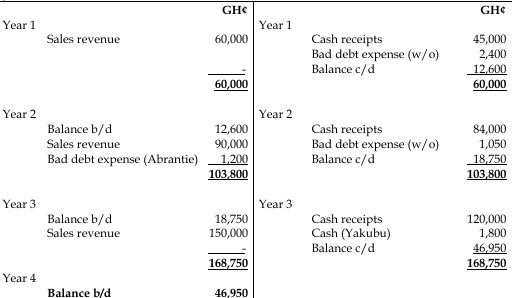

Trade Receivables Account

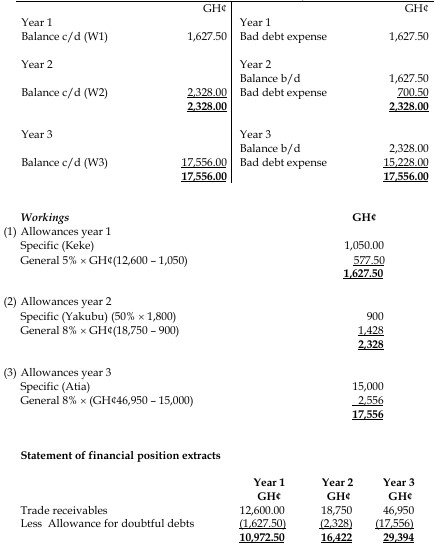

Tutorial Notes:

- Recovery of Written-Off Debts: If Abrantie’s receipt was not included in the GH¢280,000 but recorded as a receipt from a non-active customer, it should be credited directly to the bad debt expense account as a recovery.

- Allowance Adjustment: There’s no need to adjust Keke’s write-off against the allowance account, even if it was previously provided for. The previously made allowance is “released” to the expense account since it’s no longer needed.

- Provision vs. Write-Off: Since Yakubu’s debt was only provided against and not written off, a “reinstatement” adjustment would be incorrect.

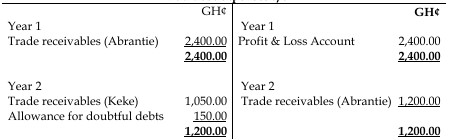

Bad debt expenses a/c

Allowance for doubtful debts a/c