Question

Answer

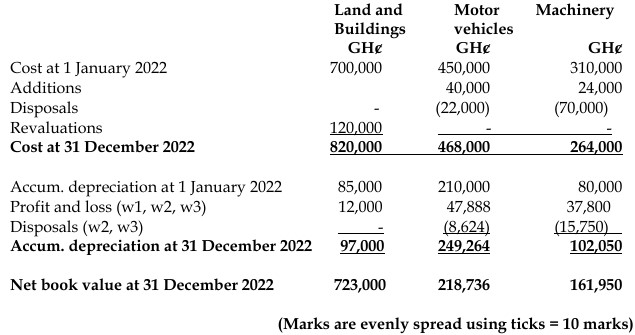

Pramso Ltd – Schedule of Non-Current Assets for the year ended 31 December 2022

1. Depreciation of buildings charged to profit and loss account:

(700,000 – 400,000) x 4% = 12,000

2. Accumulated depreciation of motor vehicle disposed of:

22,000 x 20% + (22,000 – 4,400) x 20% + (22,000 – 4,400 – 3,520) x 20% x 3/12 = 4,400 +

3,520 + 704 = 8,624.

3. Accumulated depreciation of machinery disposed of:

70,000 x 15% x 6/12 + 70,000 x 15% = 5,250 + 10,500 = 15,750.

4. Depreciation of motor vehicle charged to profit and loss account:

(428,000 – (210,000 – 7,920)) x 20% + (22,000 – 7,920) x 20% x 3/12 + 40,000 x 20% x

3/12 = 45,184 + 704 + 2,000 = 47,888.

5. Depreciation of machinery charged to profit and loss account:

(310,000 – 70,000) x 15% + 24,000 x 15% x 6/12 = 36,000 + 1,800 = 37,800