Question

Answer

a) Marginal Costing Statement of Profit or Loss for the two Quarters to 31st December 2020

| Quarter | 3 | 4 |

|---|---|---|

| GH¢ | GH¢ | |

| Sales (W1) | 550,000 | 950,000 |

| Variable cost of goods sold: | ||

| Opening Inventory | – | (67,500) |

| Production (W2) | 315,000 | 382,500 |

| Closing Inventory | (67,500) | (22,500) |

| Total Variable Production Cost | 247,500 | 427,500 |

| Non-Production Cost: | ||

| Selling & Dist. Cost | 55,000 | 95,000 |

| Total Variable Cost | (302,500) | (522,500) |

| Contribution | 247,500 | 427,500 |

| Fixed Costs: | ||

| Production | 120,000 | 120,000 |

| Non-production | 40,000 | 40,000 |

| Total Fixed Costs | (160,000) | (160,000) |

| Net profit | 87,500 | 267,500 |

b) Absorption Costing Statement of Profit or Loss for the two Quarters to 31st December 2020

| Quarter | 3 | 4 |

|---|---|---|

| GH¢ | GH¢ | |

| Sales | 550,000 | 950,000 |

| Cost of Sales: | ||

| Opening Inventory | – | (90,000) |

| Production | 420,000 | 510,000 |

| Closing Inventory | (90,000) | (30,000) |

| Total Cost of Sales | 330,000 | 570,000 |

| Gross Profit | 220,000 | 380,000 |

| Expense: | ||

| Selling & Dist. | 55,000 | 95,000 |

| Admin. Expenses | 40,000 | 40,000 |

| Total Expenses | (95,000) | (135,000) |

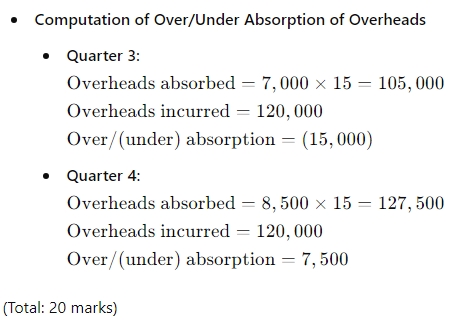

| Over / (Under) Absorption | (15,000) | 7,500 |

| Net Profit | 110,000 | 252,500 |

Workings:

- Computation of Product Cost/unit

- Marginal Costing

- Direct Material Costs: GH¢20

- Direct Labour: GH¢15

- Variable Overheads: GH¢10

- Total Product cost/unit: GH¢45

- Absorption Costing

- Direct Material Costs: GH¢20

- Direct Labour: GH¢15

- Variable Overheads: GH¢10

- Fixed Overheads: GH¢15

- Total Product cost/unit: GH¢60

- Marginal Costing