Question

Answer

a) Features of Bank Reconciliation Statement

- It is not part of the books of accounts.

- It is prepared periodically depending on the volume of transactions, such as weekly, monthly, or quarterly.

- It ensures that the cash book and bank statement balances match.

- It helps in detecting errors, fraud, or any cash manipulation. (4 marks evenly spread)

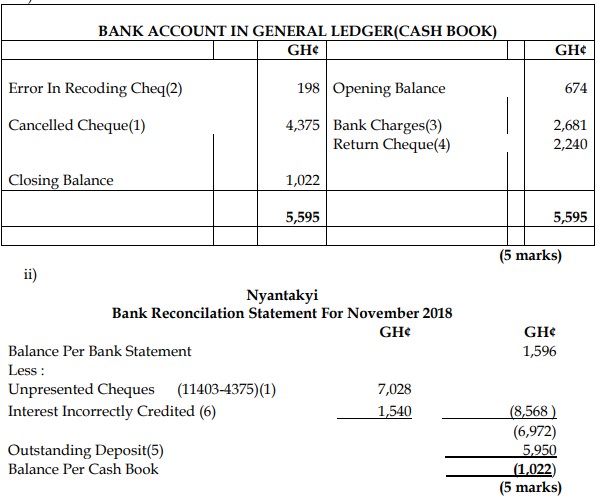

b) Adjusted Cash Book for Nyantakyi Ltd for November 2018

c) i) Errors that can be detected by the trial balance are:

Transposition

A transposition error is a simple error of data entry that occurs when two digits

that are either individual or part of a larger sequence of numbers are accidentally

reversed when posting a transaction. If one is reversed and the other is correct.

Omission (if it’s one sided)

Commission ( If one sided, or two debit entries are made)

(2 errors explained @1.5 marks each = 3 marks)

ii) Reasons for having control accounts

They provided a check on the accuracy of entries made in the personal accounts in

the receivables and payables ledger.

Control accounts also assist in the location of errors.

Where there is a separation of clerical duties, the control account provides an internal check.