Question

Answer

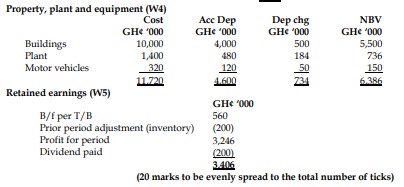

Workings:

Depreciation (W1):

- Buildings: GH¢ 10,000 x 5% = GH¢ 500

- Plant: (GH¢ 1,400 – GH¢ 480) x 20% = GH¢ 184

- Motor vehicles: (GH¢ 320 – GH¢ 120) x 25% = GH¢ 50

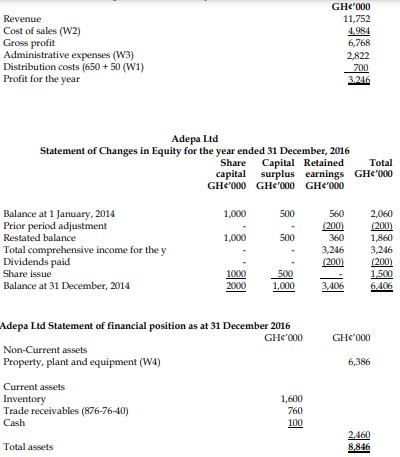

Cost of sales (W2):

- Opening inventory: GH¢ 2,200

- Purchases: GH¢ 4,200

- Depreciation – Plant: GH¢ 184

- Closing inventory: GH¢ (1,600)

- Total: GH¢ 4,984

Administrative expenses (W3):

- Per T/B: GH¢ 2,206

- Depreciation – Buildings: GH¢ 500

- Irrecoverable debt: GH¢ 76

- Receivable allowance: (GH¢ 876 – GH¢ 76) x 5% = GH¢ 40

- Total: GH¢ 2,822