Question

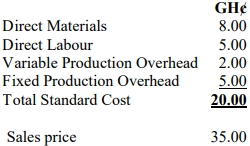

a) Resol Ltd commenced trading on 1 April 2011 making the product Resol. The standard cost sheet for Resol is as follows:

The fixed production overhead figure has been calculated on the basis of a budgeted normal output of 24,000 units per annum. Fixed Sales and Administration costs are estimated at GH¢24,000 per annum. You may assume that all budgeted fixed expenses are incurred evenly over the year.

The sales price is GH¢35.00 and the actual number of units produced and sold was as follows:

| April | May | |

|---|---|---|

| Production – units | 2,000 | 2,500 |

| Sales – units | 1,500 | 3,000 |

Required:

Prepare a profit statement for each of the months April and May using:

- Standard costing

- Absorption costing