Question

Answer

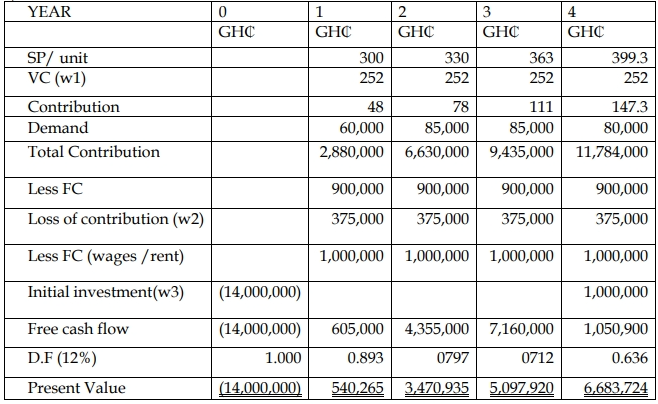

a)

NPV = 1,792,844

Recommendation: The project is acceptable in view of positive NPV

Working 1. Expected variable cost per unit = (GH¢240 x 0.4) + (260 x0.6) = GH¢252

Working 2. Loss contribution 5,000 x GH¢75 = GH¢375,000

Working 3. Initial cost – disposal (16,000,000- 2,000,000) = GH¢14,000,000