Question

Answer

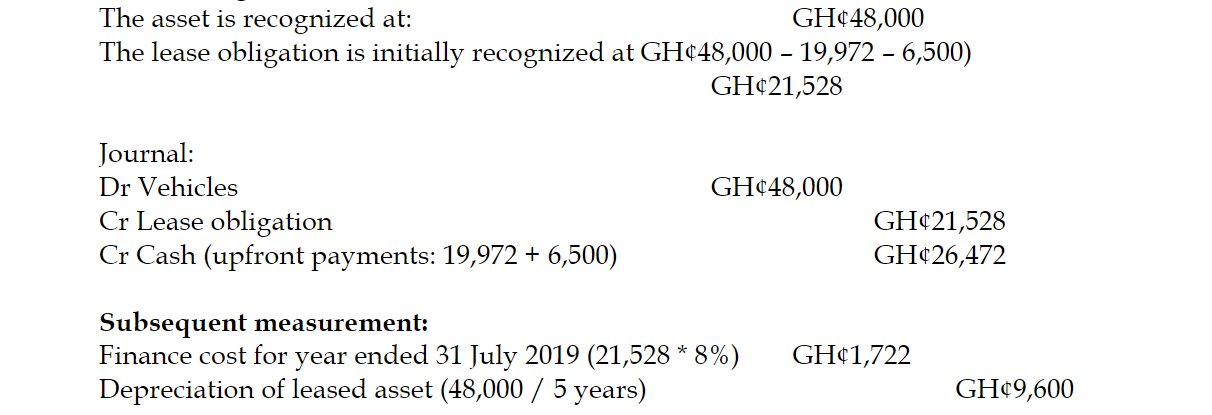

c) Workings

Initial recognition & measurement:

Journal:

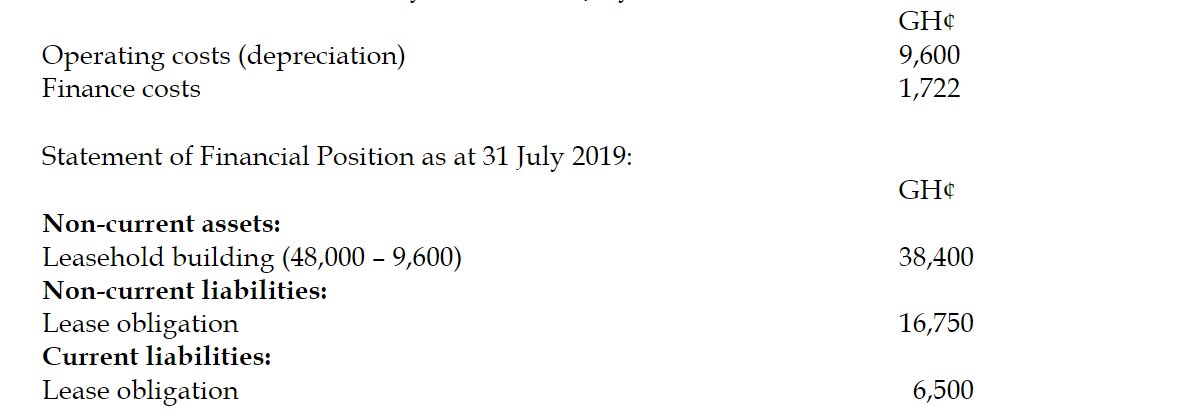

Closing balance on lease obligation (21,528 + 1,722) GH¢23,250

Presented as current liability (full payment as it is in advance, due 1 August 2019) GH¢6,500

Presented as non-current liability GH¢16,750

Extracts from financial statements for year ended 31 July 2019:

Statement of Profit or Loss for year ended 31 July 2019:

Correct entries in the Workings Schedule – 4 marks 6 correct entries in the financial statements extract – 3 marks