Question

Answer

a)

Enhancing Qualitative Characteristics:

- Comparability:

Comparability allows users to identify similarities and differences between two sets of economic phenomena. Information is more useful if it can be compared with similar information about other entities or the same entity over different periods. Consistency in application helps in achieving comparability. - Verifiability:

Verifiability ensures that different knowledgeable and independent observers could reach consensus that a particular depiction is a faithful representation. It helps to assure users that information faithfully represents the economic phenomena it purports to represent. - Timeliness:

Timeliness means having information available to decision-makers in time to be capable of influencing their decisions. Information that is available after the decision-making process is less useful. - Understandability:

Information is understandable if it is classified, characterized, and presented clearly and concisely. Financial reports should be prepared for users who have a reasonable knowledge of business and economic activities.

(4 points @ 2.5 marks each = 10 marks)

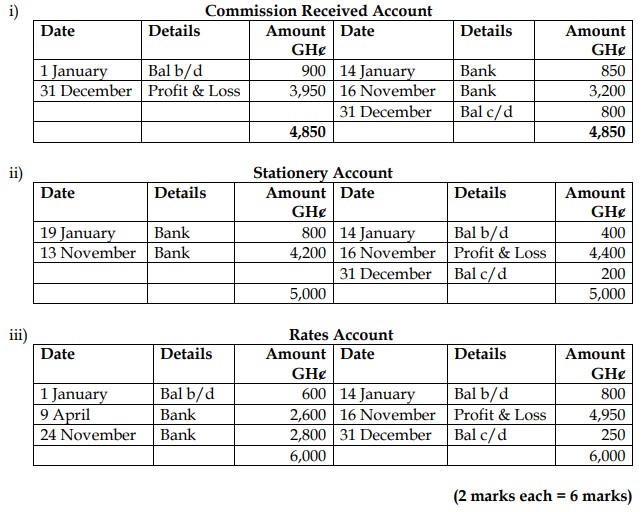

b)

c)

Reasons for Adjustments for Accruals and Prepayments:

- Accurate Reflection of Financial Position:

Adjusting for accruals and prepayments ensures that expenses and revenues are matched to the correct accounting period, providing an accurate reflection of the company’s financial position. - Compliance with Accounting Standards:

Making these adjustments ensures compliance with the accruals concept under accounting standards, which mandates that transactions be recorded in the period in which they occur, not when cash is received or paid.