Question

Answer

a)

i) The purpose and scope of financial accounting are as follows:

- Financial Accounting information is prepared by enterprises for external users. It provides information to meet their needs, such as shareholders, potential investors, banks, and suppliers. It is used to inform about the financial performance and position of the company, and it helps in preparing tax accounts.

- Financial Accounting information is normally regulated by law and accounting standards and is often audited. It requires the presentation of financial statements, including a Statement of Comprehensive Income, Statement of Financial Position, Statement of Cash Flows, Statement of Changes in Equity, and the necessary notes. (2 marks)

ii) Differences between Financial Accounting and Management Accounting:

- Financial statements from Financial Accounting are intended mainly for external users, while Management Accounting information is for internal use by management.

- Financial accounts describe the performance of a business over a specific period, whereas Management Accounting helps management record, plan, and control activities and assists in decision-making.

- Financial Accounting deals mainly with historical data, while Management Accounting can include future information, such as budgets. (6 marks)

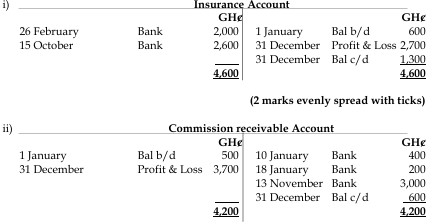

b) i) Insurance Account

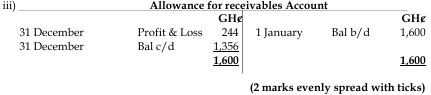

c) The prudence concept states that profits should be understated rather than overstated, and assets should be understated rather than overstated. Creating an allowance for receivables increases the expenses and reduces the profit, which is a prudent approach. It also reduces the assets, as the allowance is subtracted from receivables, making this an application of the prudence concept.

(4 marks)