Question

Answer

a) The financial statements are normally prepared on the assumption that an entity is a going concern and will continue in operation for the foreseeable future. Hence, it is assumed that the entity has neither the intention nor the need to liquidate or curtail materially the scale of its operations. Example: inventory is valued at the lower of cost or net realizable value.

(3 marks)

b) Machines:

| Quantity | Price (GH¢) | Value (GH¢) |

|---|---|---|

| Purchase | 200 | 10,000,000 |

| Sales | 150 | 9,000,000 |

| Closing Inventory | 50 |

i) If the business is forced to close down, the machines will be valued at:

| Quantity | Price (GH¢) | Value (GH¢) |

|---|---|---|

| 50 | 30,000 | 1,500,000 |

(2 marks)

ii) If the business continues, the machines will be valued at:

| Quantity | Price (GH¢) | Value (GH¢) |

|---|---|---|

| 50 | 50,000 | 2,500,000 |

(2 marks)

c) Faithful representation:

- The information gives full details of its effect on the financial statements and is only recognized if its financial effects are certain.

- Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena but must faithfully represent the phenomena that it purports to represent.

- To be faithful, financial information must be complete, neutral, and free from error. A complete report must include all information necessary for the user to understand, neutral is without bias, and finally, free from error means there should be no errors or omissions in the report.

(3 marks)

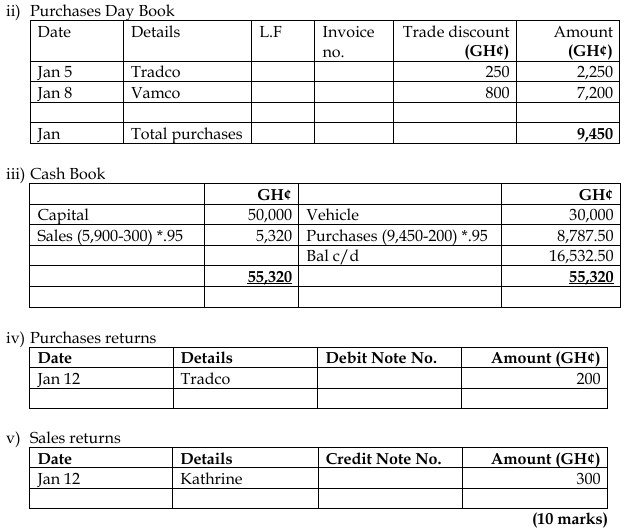

d)

i) Sales Day Book

| Date | Customer | Invoice No. | Gross Amount (GH¢) | Trade Discount (GH¢) | Net Amount (GH¢) |

|---|---|---|---|---|---|

| Jan 8 | Markcom | 5,000 | 1,000 | 4,000 | |

| Jan 8 | Kathrine | 2,000 | 100 | 1,900 |

Total Sales: GH¢5,900