Question

Answer

(a)

i. Statement of Cash flow is a statement which provides users of Financial Statement with the ability of an entity to generate cash and cash equivalents, as well as indicating the cash needs of the entity. In simple terms, it is the Statement of how cash and cash equivalents have been generated and used by an organization.

ii. Cash comprises cash on hand (physical cash) and demand deposits.

iii. Cash Equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in values.

iv. Operating Activities are the principal revenue-producing activities of the enterprise and other activities that are not investing or financing activities.

v. Investing Activities are the acquisition and disposal of non-current assets and other investments not included in cash equivalents.

vi. Financing Activities are activities that result in changes in the size and composition of the equity capital and borrowing of the entity.

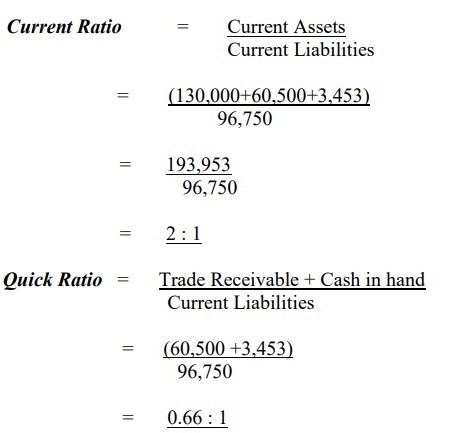

(b) (i) Calculation of Ratios

Comments: The company’s Current ratio of 2:1 is higher than the industry average of 1.55:1, while the Quick ratio of 0.66:1 is below the industry average of 0.95:1.

(ii) Liquidity/Working Capital Ratios:

- Current ratio

- Quick ratio

- Receivables collection period

- Payable payment period

- Inventory turnover period