Question

(a)

i. Define Book of Prime Entry. (1 mark)

ii. Mention any four (4) Books of Prime Entry. (4 marks)

(b) Felicia, Jackson, and Elizabeth are in Partnership Sharing Profits and Losses in the ratio of 5:3:2 respectively. According to the Partnership Agreement, Partners’ Capital Accounts attract an interest of 20% per annum, while any Drawings by a Partner also attract 10% interest per annum.

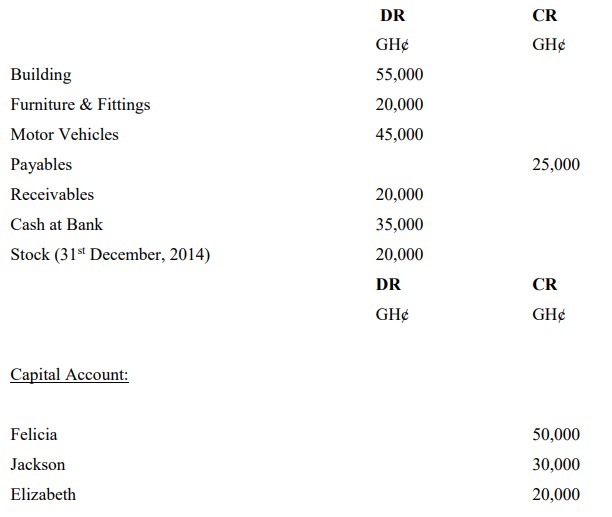

The following understated Trial Balance has been extracted after the preparation of the Profit and Loss Account for the period ending 31st December 2014:

The following entries have not been recorded in the books:

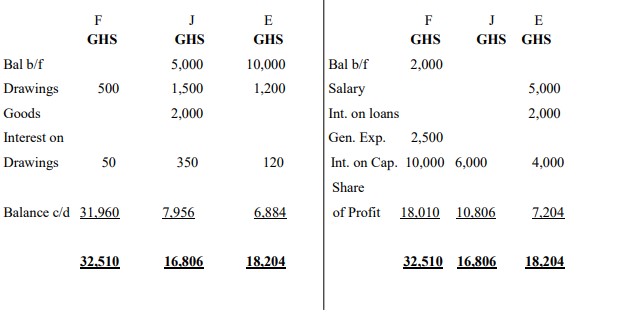

i. Salary of GH¢5,000 was paid to Elizabeth during the period.

ii. Felicia personally paid General Expenses of GH¢2,500 on behalf of the Partnership.

iii. Cash Drawings made by partners: Felicia GH¢500, Jackson GH¢1,500, and Elizabeth GH¢1,200.

iv. Interest on loan – Elizabeth – GH¢2,000.

v. Jackson took goods worth GH¢2,000 for personal use.

vi. Interest on Capital Account. All Capital Accounts were to remain fixed.

You are required to prepare:

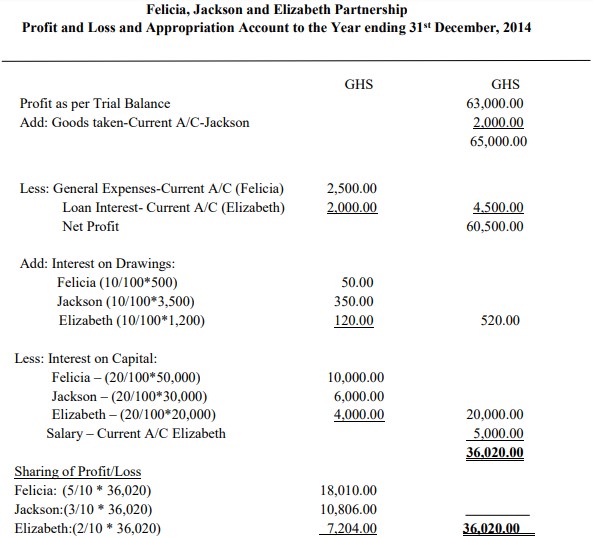

i. Profit or Loss and Appropriation Account. (7 marks)

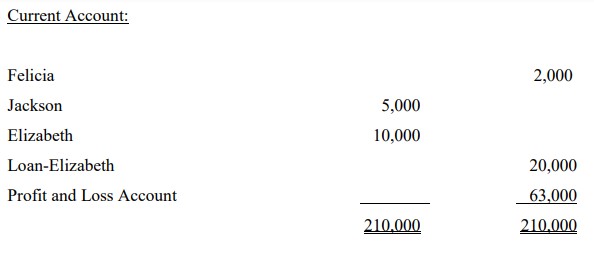

ii. Partners’ Current Account. (3 marks)

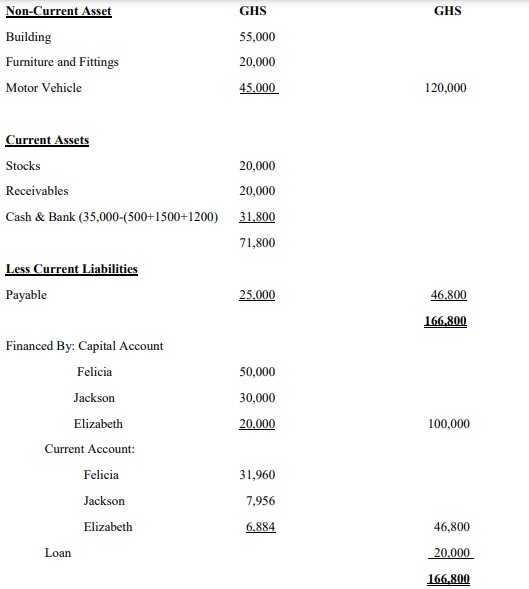

iii. Statement of Financial Position as at 31st December, 2014 (5 marks)

Answer

(a)

i. Book of Prime Entry: Books of Prime Entry are Books in which transactions are first recorded before they are posted to the ledgers.

ii. Books of Prime Entry:

- Petty Cash Book

- Cash Book

- Sales Day Book

- Sales Returns Day Book

- Purchase Returns Day Book

- Purchase Day Book

- Journal

(b) i. Profit or Loss and Appropriation Account

ii. Partners’ Current Account

iii. Statement of Financial Position as at 31st December 2014

Felicia, Jackson and Elizabeth Partnership