Question

Answer

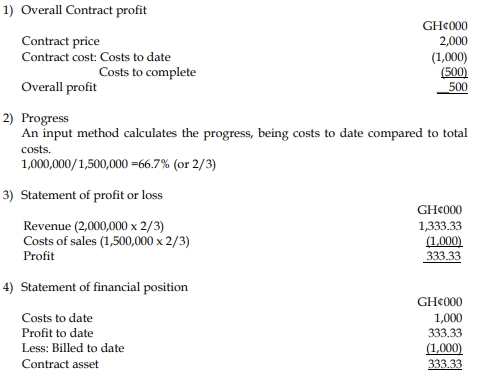

Constructing the building is a single performance obligation in accordance with IFRS 15: Revenue from Contracts with Customers.

The bonus is a variable consideration. It is excluded from the transaction price because it is not highly probable that a significant reversal in the amount of cumulative revenue recognised will not occur. The construction of the building should be accounted for as an obligation settled over time. Barikisu Ltd should recognise revenue based on progress towards satisfaction of the construction of the building.