Question

Answer

Mariam Limited will account for this transaction under the provisions of IFRS 2: Share-based Payments. IFRS 13 applies when another IFRS requires or permits fair value measurements or disclosures about fair value measurements (and measurements, such as fair value less costs to sell, based on fair value or disclosures about those measurements). IFRS 13 specifically excludes transactions covered by certain other standards, including share-based payment transactions within the scope of IFRS 2: Share-based Payment and leasing transactions within the scope of IFRS 16: Leases.

Thus, share-based payment transactions are outside the scope of IFRS 13. For cash-settled share-based payment transactions, the fair value of the liability is measured in accordance with IFRS 2 initially, at each reporting date, and at the date of settlement using an option pricing model. Unlike equity-settled transactions, the measurement reflects all conditions and outcomes on a weighted average basis. Any changes in fair value are recognised in profit or loss in the period.

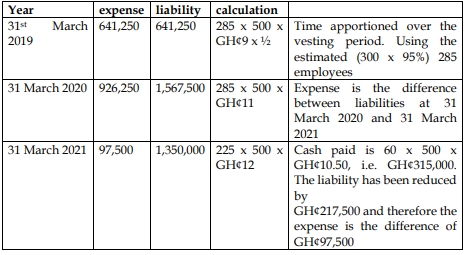

Therefore, the SARs would be accounted for as follows:

Statement of Profit or Loss for the year ended (Extracts):

| Year | Staff Costs (GH¢) |

|---|---|

| 2019 | 641,250 |

| 2020 | 926,250 |

| 2021 | 97,500 |

Statement of Financial Position Extract as at (Extracts):

| Year | SARs Liabilities (GH¢) |

|---|---|

| 2019 | 641,250 |

| 2020 | 1,567,500 |

| 2021 | 1,350,000 |