Question

Answer

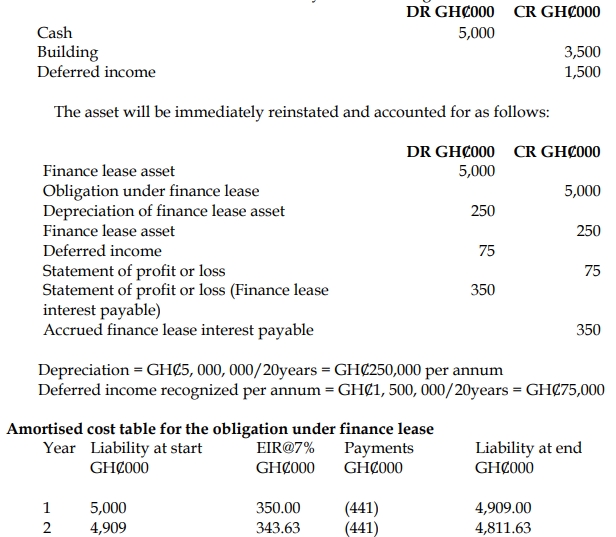

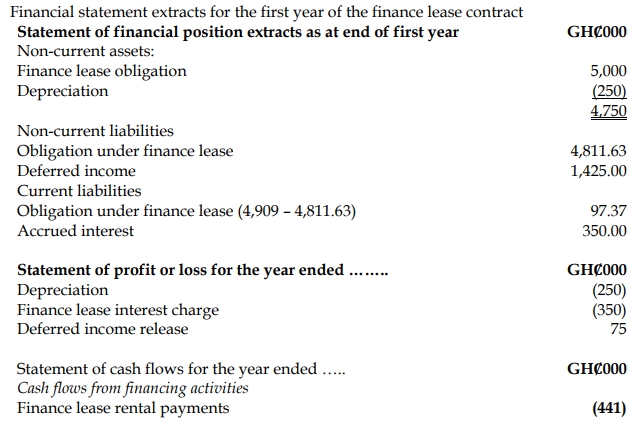

This transaction qualifies as a sale and leaseback. Given that the lease term is for the majority of the asset’s useful life and the present value of the minimum lease payments equals the fair value, the lease should be accounted for as a finance lease under IAS 17.