Question

Answer

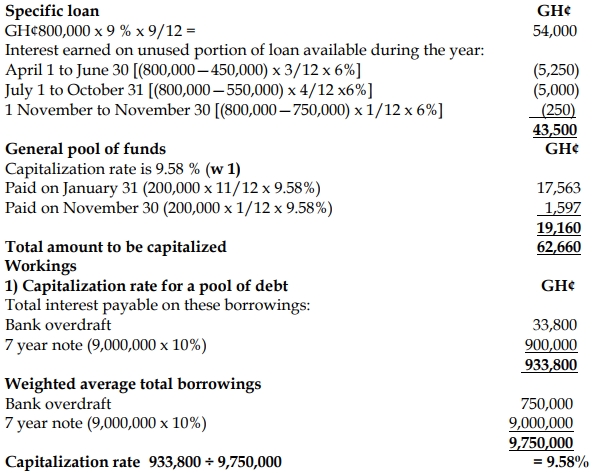

The amount to be capitalized to the cost price of the warehouse in 2014 can be calculated as follows:

Calculation

The amount to be capitalized to the cost price of the warehouse in 2014 can be calculated as follows:

Calculation