- 20 Marks

Question

The Dabi Golf Club prepares its accounts annually on 31st March. The Receipts and Payments Account for the year ended 31st March 2016 was as follows:

| GHȼ | GHȼ | |

|---|---|---|

| Balance b/d | 2,900 | |

| Subscriptions received | 70,800 | |

| Competition receipts | 12,000 | |

| Dinner dance ticket sales | 13,000 | |

| Donations | 1,000 | |

| Sale of equipment | 25,000 | |

| Competition prizes | 2,800 | |

| Groundkeepers’ wages | 14,000 | |

| Dinner dance expenses | 6,800 | |

| Insurance | 9,200 | |

| Equipment purchases | 40,000 | |

| General expenses | 30,100 | |

| Electricity | 1,400 | |

| Balance c/d | 20,400 | |

| 124,700 | 124,700 |

The following additional information is available:

i) The remaining assets and liabilities of the Club at the beginning and end of the year were:

| 1st April 2015 (GHȼ) | 31st March 2016 (GHȼ) | |

|---|---|---|

| Clubhouse | 130,000 | 130,000 |

| Equipment | 140,000 | 120,000 |

| Electricity owing | 400 | 200 |

| Subscriptions due and unpaid | 2,500 | 2,900 |

| Subscriptions paid in advance | 6,200 | 4,100 |

| Stock of competition prizes | 600 | 200 |

ii) During the year equipment with a book value of GHȼ30,000 was sold for GHȼ25,000. iii) Of the subscriptions due on 1st April 2015, GHȼ220 remains unpaid. This is to be treated as an irrecoverable debt.

Required:

a) Calculate the Accumulated Fund on 1st April 2015. (3 marks)

b) Prepare the Subscription Account for the year ended 31st March 2016. (4 marks)

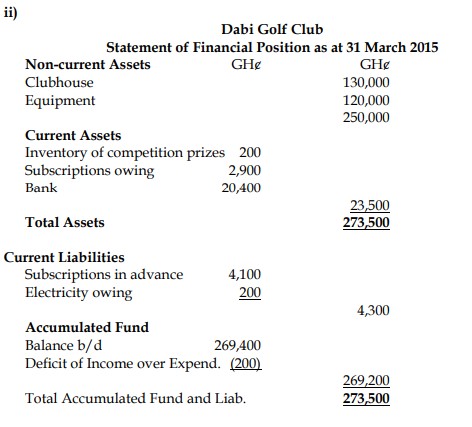

c) Prepare: i) the Income and Expenditure Account for the year ended 31st March 2016

ii) Statement of Financial Position as at 31st March 2016. (13 marks)

Answer

a)

Accumulated fund on 1 April 2015:

| GHȼ | |

|---|---|

| Clubhouse | 130,000 |

| Equipment | 140,000 |

| Bank | 2,900 |

| Stock of competition prizes | 600 |

| Subscriptions due | 2,500 |

| Total | 276,000 |

| Less: | |

| Electricity owing | 400 |

| Subscriptions in advance | 6,200 |

| 6,600 | |

| Accumulated Fund | 269,400 |

Here is the next question from the document, formatted as requested:

========== Level: Level 1 Professional Bodies: ICAG Programs: Professional Program Subjects: Financial Accounting Topics: Preparation of not-for-profit accounts Series: Nov. 2016 Total Marks: 20 Question Tags: Not-for-profit, Receipts and Payments Account, Income and Expenditure Account, Financial Position

Question Short Summary: Calculation of Accumulated Fund, preparation of Subscription Account, Income and Expenditure Account, and Statement of Financial Position for a not-for-profit organization.

Question:

QUESTION FIVE

The Dabi Golf Club prepares its accounts annually on 31st March. The Receipts and Payments Account for the year ended 31st March 2016 was as follows:

| GHȼ | GHȼ | |

|---|---|---|

| Balance b/d | 2,900 | |

| Subscriptions received | 70,800 | |

| Competition receipts | 12,000 | |

| Dinner dance ticket sales | 13,000 | |

| Donations | 1,000 | |

| Sale of equipment | 25,000 | |

| Competition prizes | 2,800 | |

| Groundkeepers’ wages | 14,000 | |

| Dinner dance expenses | 6,800 | |

| Insurance | 9,200 | |

| Equipment purchases | 40,000 | |

| General expenses | 30,100 | |

| Electricity | 1,400 | |

| Balance c/d | 20,400 | |

| 124,700 | 124,700 |

The following additional information is available: i) The remaining assets and liabilities of the Club at the beginning and end of the year were:

| 1st April 2015 (GHȼ) | 31st March 2016 (GHȼ) | |

|---|---|---|

| Clubhouse | 130,000 | 130,000 |

| Equipment | 140,000 | 120,000 |

| Electricity owing | 400 | 200 |

| Subscriptions due and unpaid | 2,500 | 2,900 |

| Subscriptions paid in advance | 6,200 | 4,100 |

| Stock of competition prizes | 600 | 200 |

ii) During the year equipment with a book value of GHȼ30,000 was sold for GHȼ25,000. iii) Of the subscriptions due on 1st April 2015, GHȼ220 remains unpaid. This is to be treated as an irrecoverable debt.

Required: a) Calculate the Accumulated Fund on 1st April 2015. (3 marks) b) Prepare the Subscription Account for the year ended 31st March 2016. (4 marks) c) Prepare: i) the Income and Expenditure Account for the year ended 31st March 2016 ii) Statement of Financial Position as at 31st March 2016. (13 marks)

(Total: 20 marks)

Answer:

a)

Accumulated fund on 1 April 2015:

| GHȼ | |

|---|---|

| Clubhouse | 130,000 |

| Equipment | 140,000 |

| Bank | 2,900 |

| Stock of competition prizes | 600 |

| Subscriptions due | 2,500 |

| Total | 276,000 |

| Less: | |

| Electricity owing | 400 |

| Subscriptions in advance | 6,200 |

| Total | 6,600 |

| Accumulated Fund | 269,400 |

(3 marks)

b)

Subscriptions Account for the year ended 31 March 2016

| GHȼ | GHȼ | |

|---|---|---|

| Balance b/d | 2,500 | |

| Income and expenditure | 73,520 | |

| Balance c/d | 4,100 | |

| Bank | 70,800 | |

| Irrecoverable debt | 220 | |

| Balance c/d | 2,900 | |

| 80,120 | 80,120 |

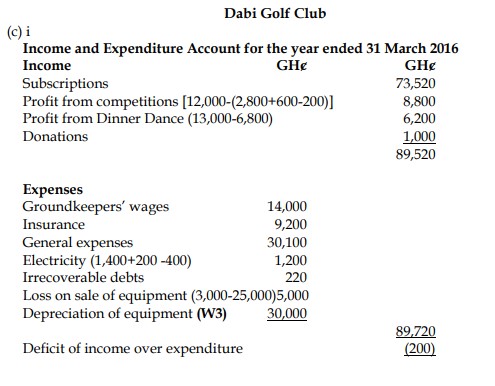

c) i) Dabi Golf Club Income and Expenditure Account for the year ended 31 March 2016

Working (W)

Depreciation calculation:

Net book value of equipment at 1 April 2014: GHȼ140,000

Disposal: (30,000)

Additions: 40,000

Net book value of equipment at 31 March 2015: (120,000)

Depreciation of equipment: 30,000

- Topic: Preparation of not-for-profit accounts

- Series: NOV 2016

- Uploader: Theophilus