Question

Answer

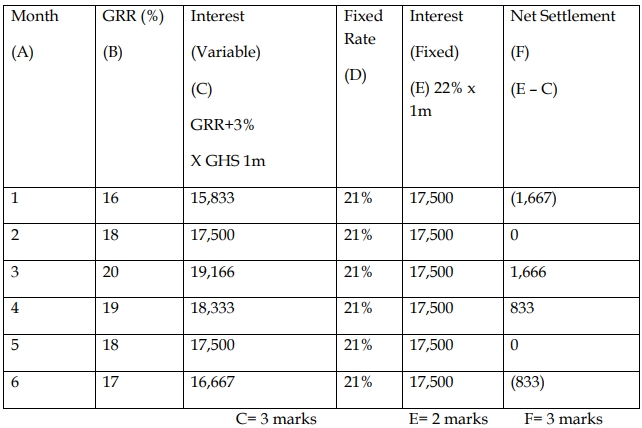

i) Calculation of Variable Interest, Fixed Interest, and Net Settlement:

ii) Interest Rate Hedge Explanation:

Yes, this strategy can be described as an interest rate hedge. The variable rate that Asanka will receive under the swap agreement compensates for the variable rate it has to pay to its original lender, North East Bank. This effectively leaves Asanka with a fixed interest payment of 21%, thereby removing the uncertainty and volatility in its monthly interest payments.

(2 marks)