Question

Answer

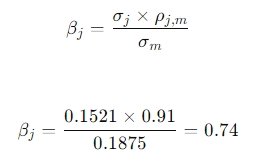

i) Equity beta:

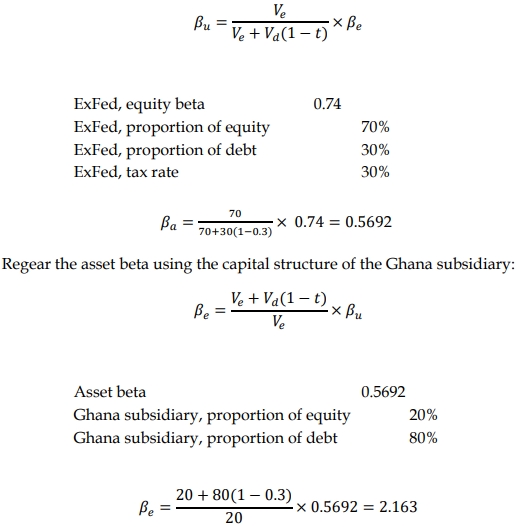

ii) Appropriate equity beta for Fameko’s subsidiary:

Since Fameko’s subsidiary would be carrying out a similar business, the level of business risk will be the same as that of ExFed. However, since the capital structure of the subsidiary will differ from that of ExFed, the financial risk will also differ. We can derive an appropriate equity beta for Fameko’s subsidiary by un-gearing the equity beta of ExFed and then re-gearing it to reflect the capital structure of the subsidiary:

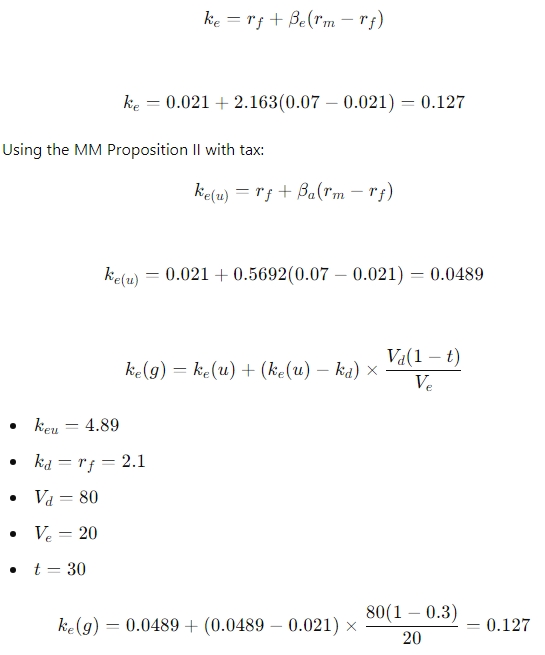

iii) The appropriate required rate of return on the equity of the Ghana subsidiary:

Using CAPM: