Question

Answer

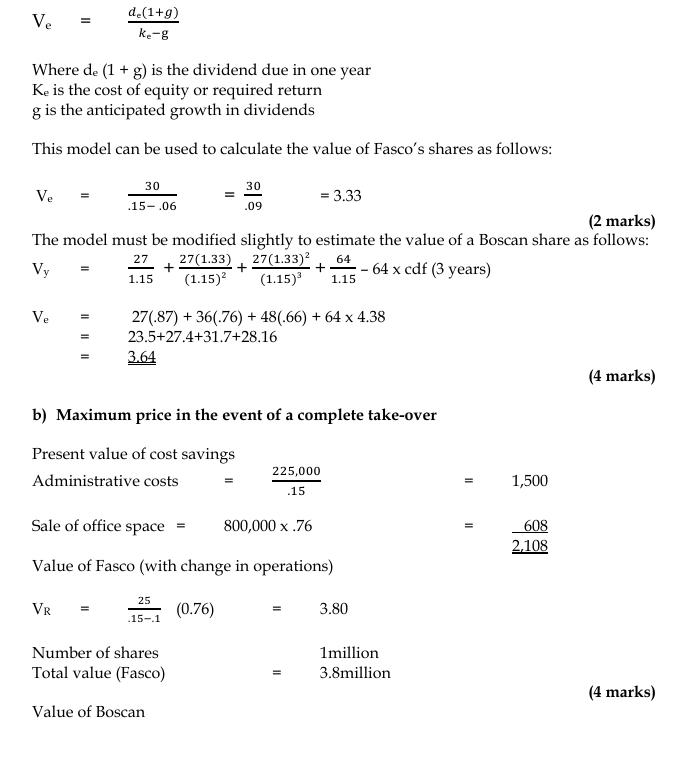

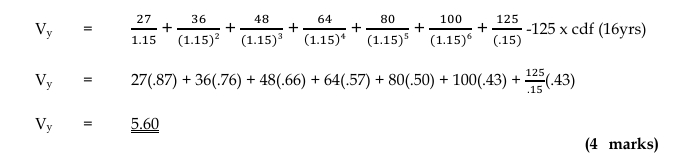

Valuation per share for a minority investment

Using the dividend valuation model (DVM), the value of ordinary shares is given by:

c) Limitations of the Approach

- Dividend Growth Assumptions: The dividend valuation model assumes that dividends grow at a constant rate indefinitely, which may not hold in real-life scenarios. Boscan’s variable dividend growth complicates the model.

- Market Conditions: The model does not account for the short-term market factors or price-earnings ratio that may affect stock prices.

- Synergies: The assumed synergies and cost savings may not materialize in practice, affecting the overall valuation.

Other factors to consider include:

- Management changes after acquisition.

- Competitive responses in the market.

- Financing options and capital structure post-acquisition.