Question

Answer

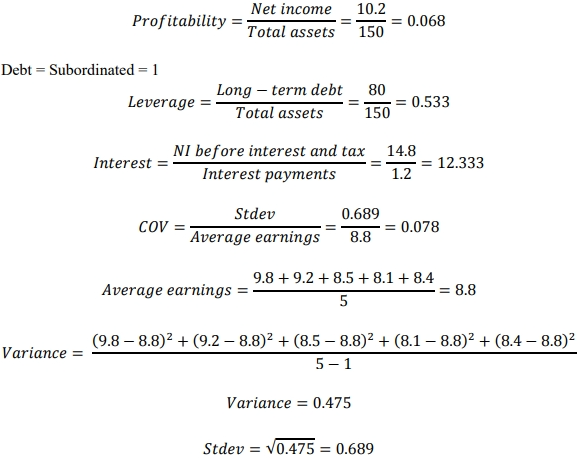

Calculate credit score (Y) using Kaplan Urwitz model for unlisted companies

𝑌 = 4.41 + 0.001𝑆𝑖𝑧𝑒 + 6.40𝑃𝑟𝑜𝑓𝑖𝑡𝑎𝑏𝑖𝑙𝑖𝑡𝑦 − 2.56𝐷𝑒𝑏𝑡 − 2.72𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒

+ 0.006𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 − 0.53𝐶𝑂V

Where

Size is measured by total assets

Profitability is measured by the ratio of net income to total assets

Debt refers to the status of the debt stock; subordinated debt is assigned score 1, and

unsubordinated debt is assigned score 0

Leverage is measured by the ratio of long-term debt to total assets

Interest refers to interest cover, which is measured by net operating income (i.e. net

income before interest and tax)

COV is the coefficient of variation in earnings, which measures volatility in earnings

𝑆𝑖𝑧𝑒 = 𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 = 200

Note: Since company has been operating since 1990, earnings record for the past five

years is a sample of earnings. The standard deviation is therefore estimated as a sample

standard deviation.

𝑌 = 4.41 + 0.001(150) + 6.40(0.068) − 2.56(1) − 2.72(0.533) + 0.006(12.333)− 0.53(0.078)

𝑌 = 1.018

With a credit score of 1.018, Lolonyo falls into the BB credit rating.

The yield on 10-year corporate bonds with BB rating is 25.5%.

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡 = 𝑌𝑇𝑀 × (1 – 𝑡𝑎𝑥 𝑟𝑎𝑡𝑒)

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡 = 25.5% × (1 – 0.25) = 19.125%

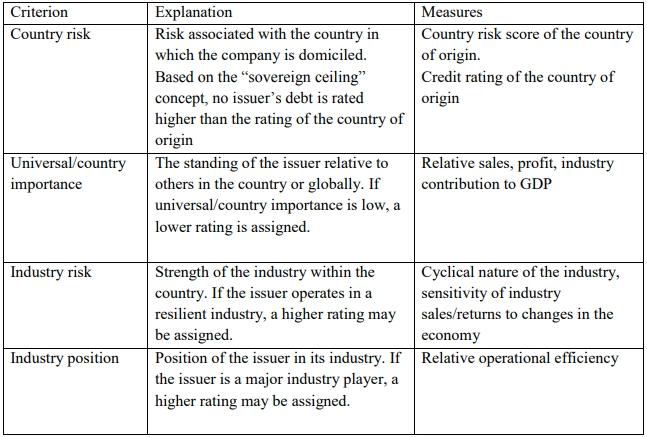

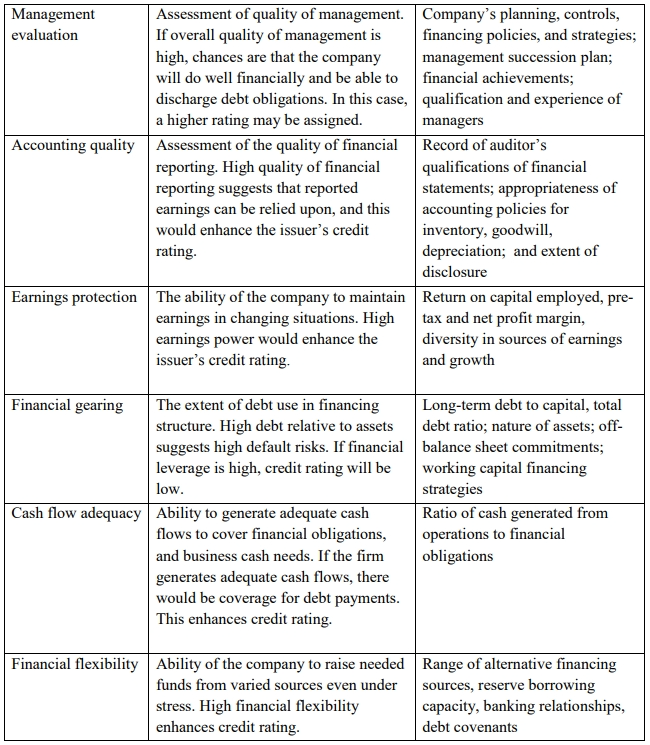

(b) Criteria used for credit rating

Criteria normally used by credit rating agencies in establishing credit rating of companies

include the following:

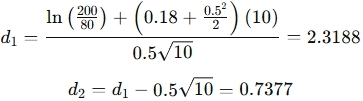

(c) Default Probability and Expected Loss:

(i) Default Probability:

Default probability is calculated using the Black-Scholes model:

Using the cumulative normal distribution, N(d2) = 0.7704.

Default probability = 1 – N(d2) = 0.2296 or 22.96%.

(ii) Expected Loss:

Expected loss is calculated as:

Loss given default = GHS80m x (1 – 0.60) = GHS32m.

Expected loss = GHS32m x 0.2296 = GHS7.3472m.