Question

Answer

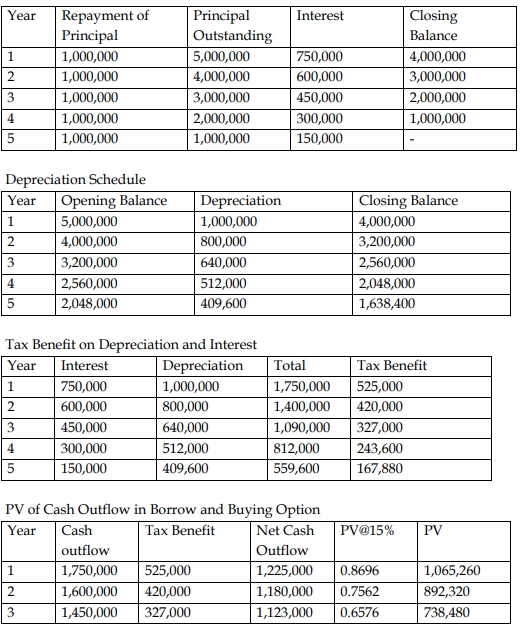

Total Present Value of Buy Option: 3,864,110

Recommendation

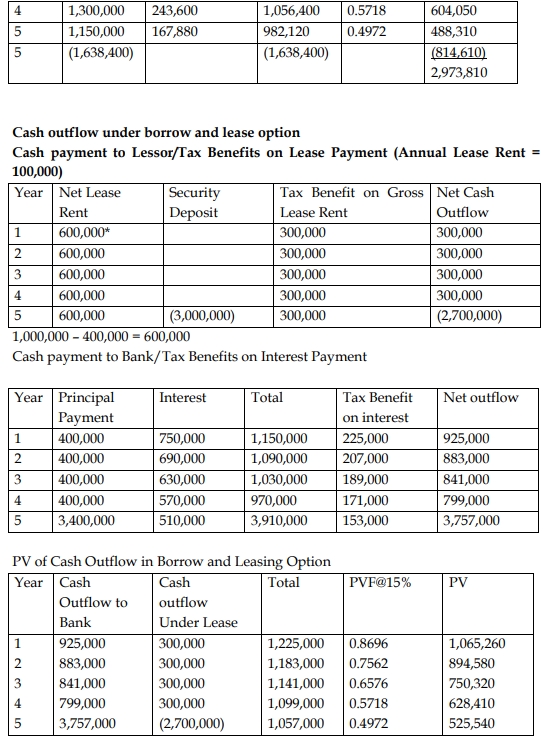

The present value of the lease option (GH¢2,011,440) is lower than the buy option (GH¢2,973,810). Therefore, the lease option is more viable for Rahim Ltd.

(10 marks evenly spread)