Question

Your audit and assurance firm has just accepted a financial statement audit engagement from Lunch Special Ltd., a restaurant that prepares lunch for the general public and on special orders. The company operates at a number of sales points in the city.

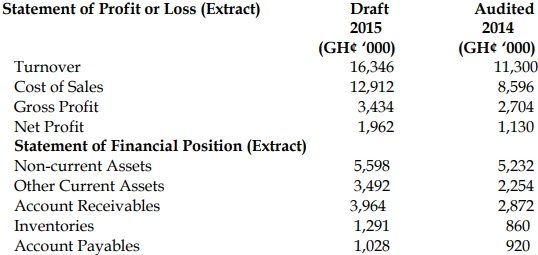

The company uses a computerised system that has networked all the Sales Points to its Head Office. Your firm is planning the new audit and has received the draft financial statements for the year. As the audit senior to lead the engagement team, you are examining the financial statements, an extract of which is shown below:

Required:

i) Using analytical procedures at the planning stage, state your observations drawn from the extracts from the draft financial statements and how they may impact your audit of the Accounts Receivables. (10 marks)