Question

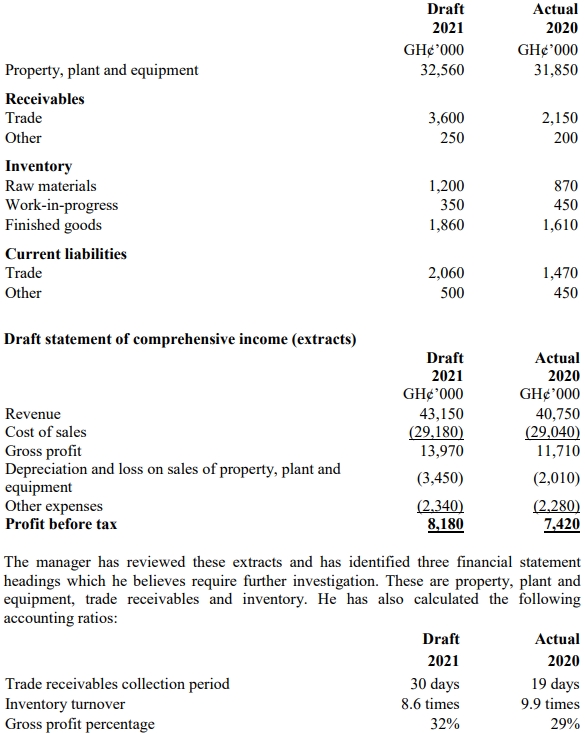

Maggie Manufacturing is a long-established manufacturing company. The audit manager has been provided with the following extracts from the draft financial statements for 2021, prior to the final audit planning meeting with the financial controller.

Draft Statement of Financial Position (Extracts):

The manager has reviewed these extracts and has identified three financial statement headings that require further investigation: property, plant, and equipment, trade receivables, and inventory. He has also calculated certain accounting ratios.

Required:

a) Explain why the manager has selected these three headings for further investigation.

b) Detail and explain the further information that the manager should request from the financial controller at the final audit planning meeting to clarify the situation with regards to the three financial statement headings.