Question

Answer

a)

i) Material Mix Variance

Flour (96,000 – (5/10 x 218000)@GH¢2.5 = 32,500 F

Sugar (72,000 – (3/10 x218,000)@GH¢ 3.0 = 19,800 A

Butter (50,000 – (2/10 X 218,000) @GH¢2.0 = 12,800 A

Total Material Mix Variance 100A

ii) Material Yield Variance

Flour (109,000 – 120,000) @GH¢2.5 = 27,500F

Sugar (65,400 – 72,000) @GH¢3.0 = 19,800F

Butter (43,600 – 48,000) @ GH¢2.0 = 8,800F

Total Material Yield 56,100F

iii) Material Usage variance = Mixed Variance + Yield Variance

Flour = 32,500 F + 27,500F = 60,0000 F

Sugar =19,800A + 19,800F = –

Butter = 12,800 A +8,800F = 4,000 A

Total 100A + 56,100F 56,000 F

Alternatively, it can be calculated as:

| Ingredient | Actual Usage (Kg) | Standard Usage (Kg) | Standard Cost (GH¢) | Usage Variance (GH¢) |

|---|---|---|---|---|

| Flour | 96,000 | 120,000 | 2.50 | 60,000 F |

| Sugar | 72,000 | 72,000 | 3.00 | – |

| Butter | 50,000 | 48,000 | 2.00 | 4,000 A |

| Total Usage Variance | 56,000 F |

(3 marks)

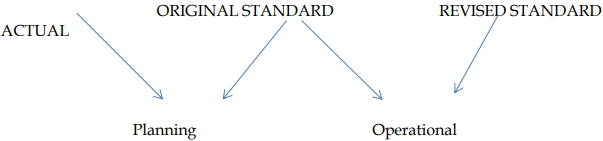

b) Planning Variances vs. Operational Variances:

- Planning Variance: A planning variance, also known as a revision variance, compares an original standard with a revised standard that would have been used if the planner had known what was going to happen. It reflects the difference between the budgeted amounts and the amounts that should have been budgeted given the actual circumstances.

- Operational Variance: An operational variance compares actual results with the revised standard. It focuses on the efficiency of management in controlling costs and operations under the conditions that actually prevailed during the period.

(2 marks)

c) Importance of Separating Variances into Planning and Operational Components:

- Identifies Control Issues: Separating variances into planning and operational components allows management to distinguish between variances caused by factors outside their control (planning variances) and those that are within their control (operational variances).

- Improved Decision Making: It enables management to focus on the controllable aspects of the business, leading to better decision-making and more effective resource allocation.

- Motivates Managers: By focusing on operational variances, managers are more likely to be motivated to improve efficiency, knowing that they are not being judged on factors beyond their control.

- Improves Planning Processes: Planning variances can highlight weaknesses in the budgeting process, leading to improvements in future planning and forecasting.

(4 marks)