Question

Answer

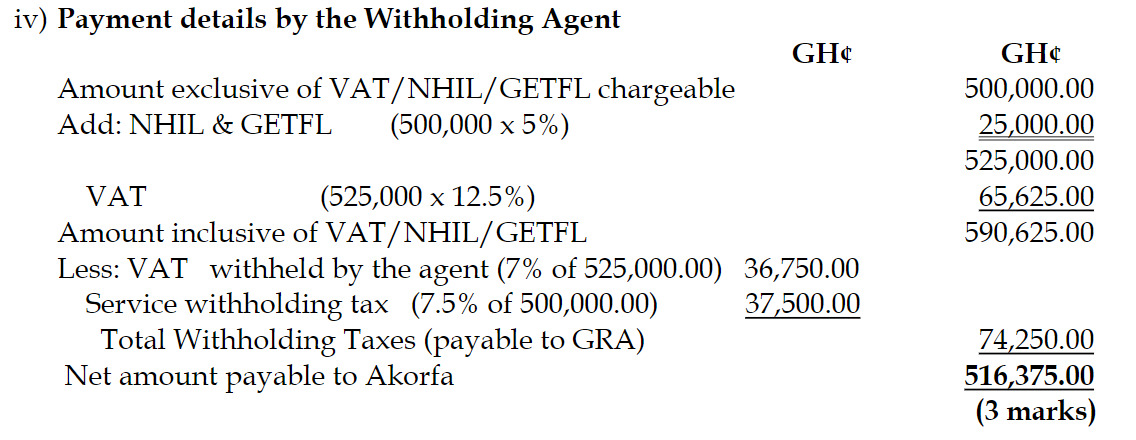

i) Proportion of VAT that should be withheld by the agent:

Proportion of VAT to be withheld (7% x 525,000) GH¢36,750

(3 marks)

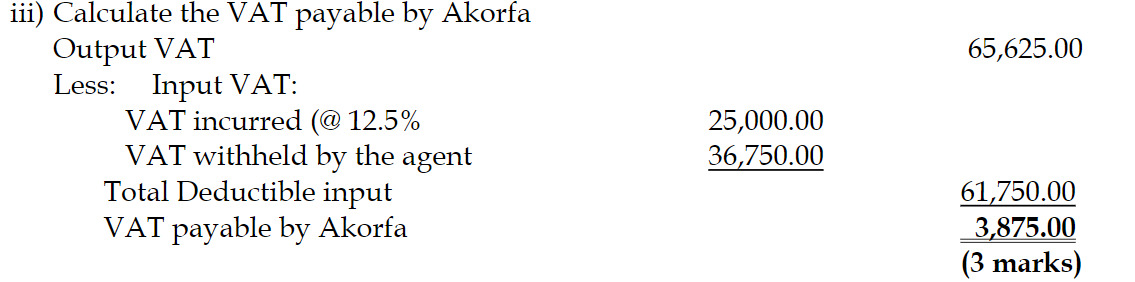

ii) Calculation of output VAT:

Description Amount (GH¢)

12.5% x 525,000 65,625.00

Output VAT GH¢65,625

(3 marks)