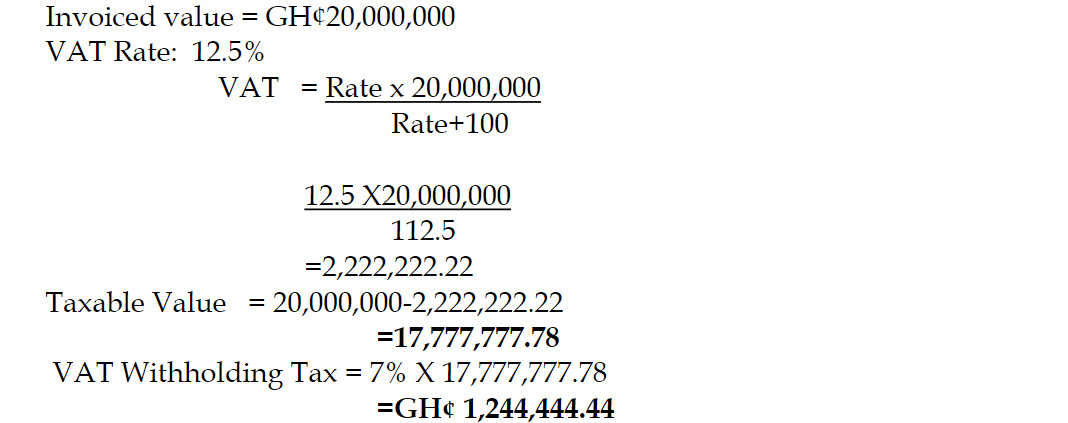

- 5 Marks

Question

State whether the following are taxable or not and briefly explain your answer.

i) Hostel facility offered to candidates by the Commonwealth Hall of the University of Ghana for profit.

ii) The supply of food and drinks by Papaye to the Vice President of Ghana for the celebration of his birthday.

Answer

i) Hostel facility offered to candidates by the Commonwealth Hall of the University of Ghana for profit

The provision of hostel facilities for profit is considered a taxable supply under the VAT Act, 2013 (Act 870). Commonwealth Hall offering hostel accommodation for profit is regarded as a commercial activity and therefore subject to VAT. It becomes exempt from VAT only if the purpose is not for profit, such as in cases of hosting candidates for educational purposes without a profit motive.

ii) Supply of food and drinks by Papaye to the Vice President of Ghana for the celebration of his birthday

The supply of food and drinks to the Vice President of Ghana for his birthday celebration is taxable. The Vice President, unlike the President of Ghana, does not have any specific exemptions or reliefs under VAT law. Therefore, this transaction is subject to VAT as it involves the supply of goods and services for consumption.

- Tags: Food Supply, Hostel Facility, Taxable Transactions, VAT

- Level: Level 2

- Topic: Value-Added Tax (VAT), Customs, and Excise Duties

- Series: NOV 2023

- Uploader: Cheoli