Question

Answer

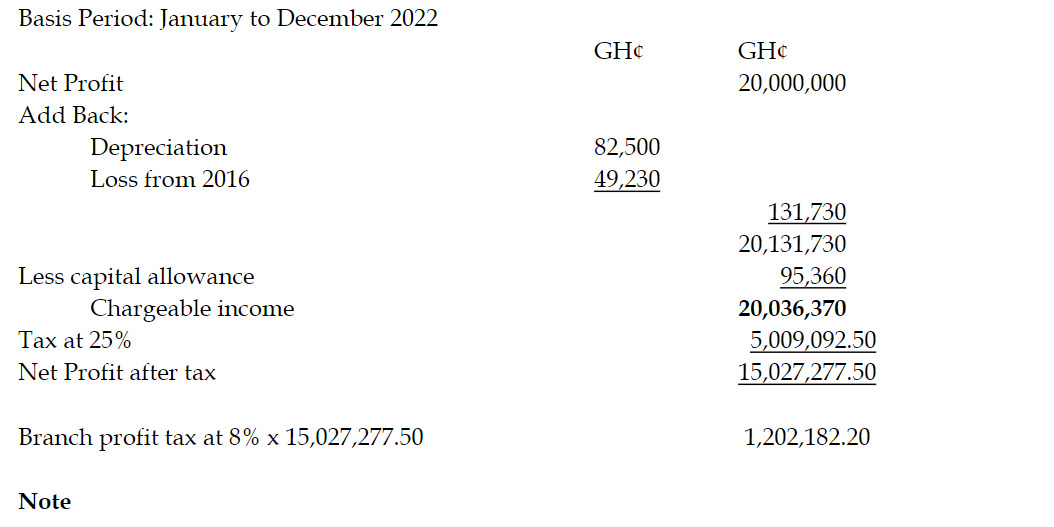

There was a loss of GH¢500,000 from 2020, but no instruction was provided regarding its treatment. It was assumed the loss was offset in the prior year.

(10 marks)