Question

Answer

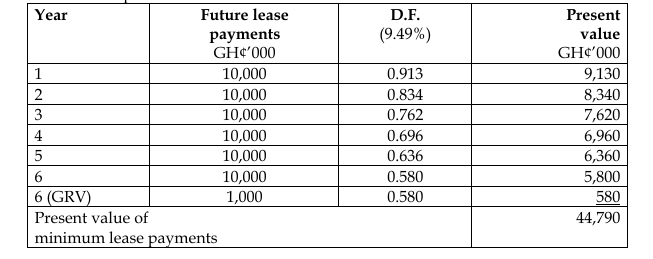

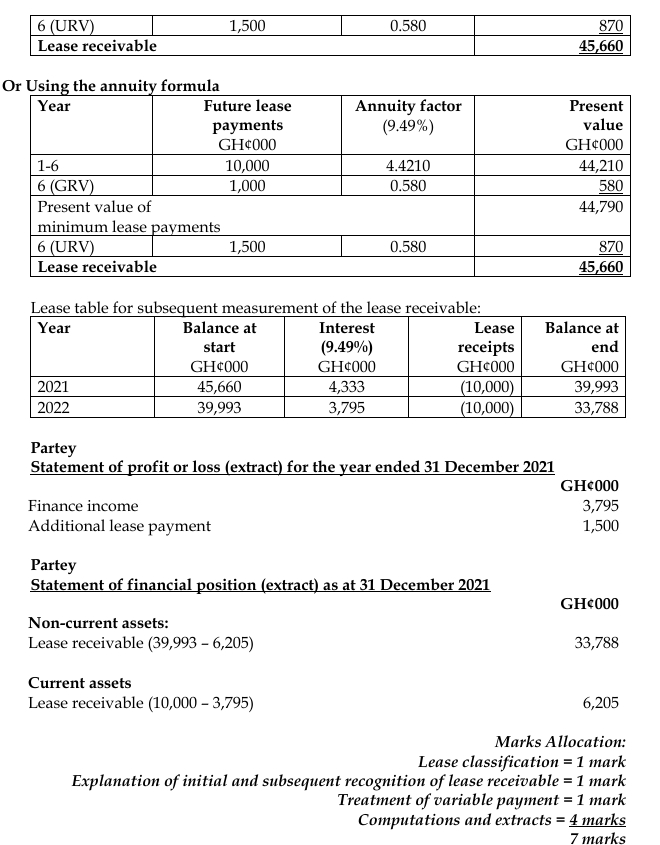

Partey would account for the lease agreement as a finance lease based on the following reasons: The lease term of six years occupies more than 75% of the equipment’s useful economic life of seven years; Mane, the lessee, is responsible for insuring and maintaining the equipment; and The underlying asset is custom-made. At the initial recognition date, Partey would recognise a lease receivable for the finance lease. The receivable would be initially measured at either the sum of the equipment’s fair price and lessor’s initial direct costs or the present value of minimum lease payments and unguaranteed residual value, and subsequently adjusted for interest income, lease payments, any required re-measurements and impairment (if any).

The lease payments would exclude the variable payment as the variability depends on management’s own performance. Partey would only account for such payment as income if the predefined condition is met: