- 14 Marks

Question

Last Chance Limited operates various manufacturing and retail operations throughout Ghana and has 400 million GH¢0.25 ordinary shares in issue. For the year that has just ended, the directors reported total after-tax profits of GH¢300 million and the P/E ratio of the company is 11.4 times.

The company has developed sophisticated computer software over the years and now considers ‘spinning-off’ its subsidiary, Ananse Systems Limited. Ananse Systems Limited has contributed GH¢40 million of the total after-tax profits of Last Chance Limited. After the spin-off, Last Chance Limited’s P/E ratio is expected to reduce to 11.0 times, while Ananse Systems Limited is expected to attract a P/E ratio of either 17 or 18 times.

Required:

i) Suggest THREE reasons why Last Chance Limited may wish to ‘spin-off’ part of its operations. (3 marks)

ii) Discuss THREE possible disadvantages of a ‘spin-off’ for the shareholders of Last Chance Limited. (3 marks)

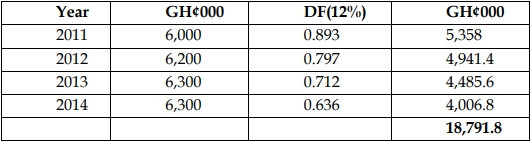

iii) Calculate the likely effect of the proposed ‘spin-off’ on the wealth of a shareholder holding 10,000 ordinary shares in Last Chance, assuming that Ananse Systems Limited trades at a P/E ratio of 17 times and 18 times. (8 marks)

(Ignore taxation)

Answer

i) Three reasons for ‘spin-off’:

- Market sentiment: Investors may feel more confident in separate, specialized companies rather than a conglomerate, increasing shareholder value.

- Market valuations: The market may undervalue a particular operation. A spin-off can help unlock the value of that operation.

- Strategic objectives: Directors may wish to focus on the core business, spinning off non-core operations for better strategic alignment.

(3 marks)

ii) Three disadvantages of ‘spin-off’:

- Increased vulnerability to takeover: After the spin-off, Last Chance may become a smaller, more attractive acquisition target.

- Reduced ability to raise finance: A smaller company post-spin-off may struggle to raise finance through debt or equity.

- Loss of economies of scale: With reduced size, Last Chance may lose advantages like bulk purchasing and shared administrative costs.

(3 marks)

iii) Effect of spin-off on shareholder wealth:

- Before spin-off:

Value of one share in Last Chance Ltd = GH¢300 million × 11.4 / 400 million = GH¢8.55

Value of 10,000 shares = 10,000 × GH¢8.55 = GH¢85,500 - After spin-off:

Earnings available to Last Chance Ltd after spin-off = GH¢300 million – GH¢40 million = GH¢260 million

Value of one share in Last Chance Ltd after spin-off = GH¢260 million × 11.0 / 400 million = GH¢7.15

Value of 10,000 shares = 10,000 × GH¢7.15 = GH¢71,500

Ananse Systems Ltd (P/E ratio of 17 times):

Value of one share in Ananse Systems = GH¢40 million × 17 / 64 million = GH¢10.625

Value of 10,000 shares = (1/8 × 10,000) × GH¢10.625 = GH¢13,281

Total wealth of the shareholder = GH¢71,500 + GH¢13,281 = GH¢84,781

Ananse Systems Ltd (P/E ratio of 18 times):

Value of one share in Ananse Systems = GH¢40 million × 18 / 64 million = GH¢11.25

Value of 10,000 shares = (1/8 × 10,000) × GH¢11.25 = GH¢14,062

Total wealth of the shareholder = GH¢71,500 + GH¢14,062 = GH¢85,562

Comment on findings:

The shareholder’s wealth after the spin-off is nearly equal to or slightly higher than before the spin-off, indicating a marginal benefit at best. There is a risk that shareholder wealth could be reduced, depending on the P/E ratio achieved by Ananse Systems.

- Tags: Corporate finance, P/E Ratio, Shareholder Wealth, Spin-off, Stock Market, Valuation

- Level: Level 3

- Topic: Business reorganisation, Valuation of acquisitions and mergers

- Series: NOV 2016

- Uploader: Joseph