- 3 Marks

Question

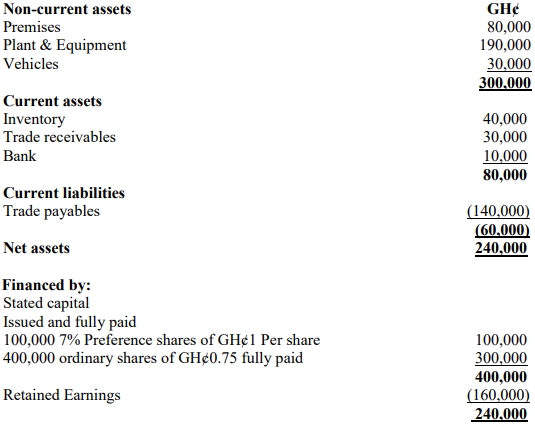

Management of Kwame Enterprise Ltd considers increasing its stated capital by transferring GH¢600,000 from Income Surplus in 2019 year of assessment in its bid to expand its business horizon in future. The management of the company intends to consult widely on the taxability, if any, on this line of action.

Required:

Assess the tax implication of this funding arrangement by Management of Kwame Enterprise Ltd.

(3 marks)

Answer

The Management of Kwame Enterprise Limited’s proposal to increase its stated capital will have to be given a legal effect. This arrangement therefore will require a payment of stamp duty. The stamp duty, which is a direct tax, is calculated at the rate of 0.5% of the amount of stated capital. In this case, the amount of stamp duty is (0.5% x 600,000) = GH¢3,000.00. The transfer from income surplus shall be treated as dividend with withholding tax at the rate of 8% imposed on the transfer. Management of Kwame Enterprise Ltd shall pay an amount of three thousand Ghana cedis as stamp duty to Ghana Revenue Authority through the Registrar General Department before the proposed transaction will take legal effect and an amount of forty-eight thousand Ghana cedis as dividend withholding tax.

- Tags: Dividend Withholding Tax, Income Surplus, Stamp Duty, Stated Capital

- Level: Level 3

- Topic: Tax administration in Ghana

- Series: MAY 2019

- Uploader: Cheoli