Question

Answer

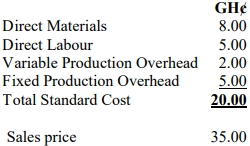

Standard Cost Card for One Door:

Per Unit

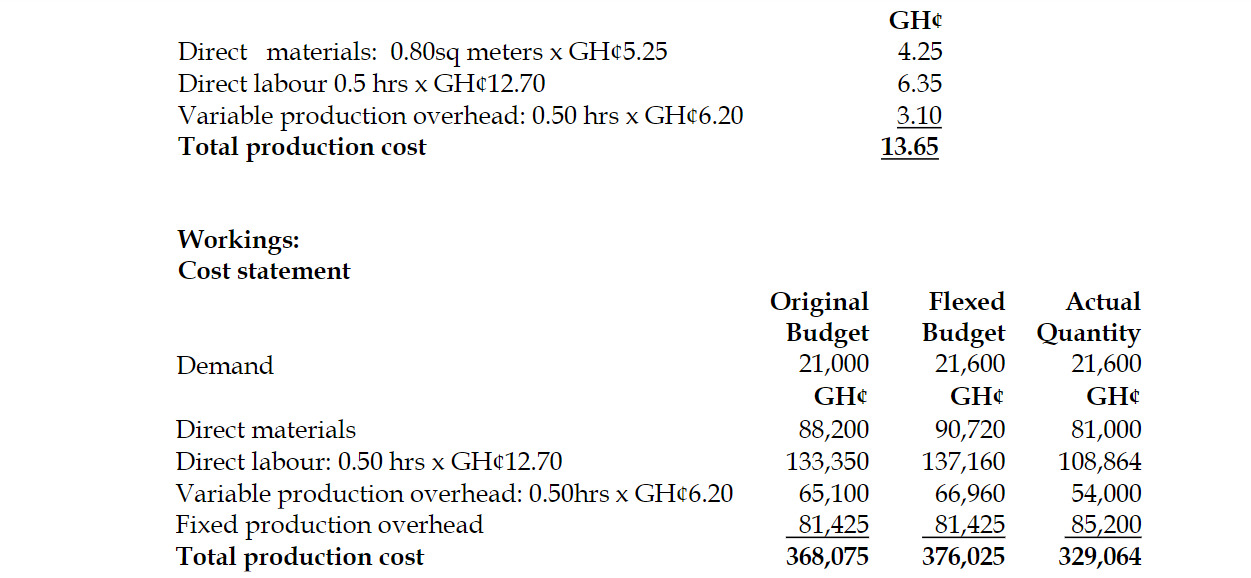

Materials price variance

= (SP – AP) x AQ = GH¢4,050

= (SP – GH¢81,000/16,200) x 16,200 = GH¢4,050

=> 16,200 SP = GH¢81,000+GH¢4,050

=>SP = GH¢ 5.25 per square metre

Materials usage variance

= (SQ – AQ) x SP = GH¢5,670

= (SQ – 16,200) x GH¢5.25 = GH¢5,670

=> 5.25 SQ = GH¢85,050 + GH¢5,670

=> SQ = 17,280 square metres

SQ = Total standard materials quantity for actual production

=> need to get standard quantity to produce one unit

= 17,280 square metres / 21,600 units = 0.80 square metres per unit

Labour efficiency variance

= (SH – AH) x SR = GH¢ 27,432

= (SH – 8,640) x GH¢12.70 = GH¢ 27,432

=> 12.70 SH = GH¢109,728 + GH¢27,432

=> SH = 10,800 hours

SH = Total standard hours required for actual production

=> need to get standard quantity to produce one unit

= 10,800 / 21,600 units = 0.5 hours per unit

Variable overhead expenditure variance

= (SR – AR) x AH = -GH¢432

= (SR – GH¢54,000/8,640) x 8,640 = -GH¢432

=>8,640 SR = GH¢54,000 – GH¢432

=>SR = GH¢ 6.20 per hour

Variable overhead efficiency variance

= (SH – AH) x SR = GH¢13,392

= (SH – 8,640) x GH¢6.20 = GH¢13,392

=> 6.20 SH = GH¢53,568 + GH¢13,392

=> SH = 10,800

Variable overhead is applied to products based on labour hours

=> standard quantity to produce one unit = 0.50 hours

Fixed production overhead expenditure variance

= (BFO – AFO) = (GH¢3,775)

= (BFO – GH¢85,200) = (GH¢3,775)

=> BFO = GH¢85,200 + (GH¢3,775)

=> BFO = GH¢81,425

(10 marks)