Question

Answer

a) Differences between a company and a partnership

- Legal Status:

- Company: A company has a separate legal identity from its owners (shareholders). It can own property, sue and be sued in its own name.

- Partnership: A partnership does not have a separate legal identity. Partners are jointly and severally liable for the debts of the partnership.

- Liability:

- Company: Shareholders have limited liability, meaning they are only liable for the amount unpaid on their shares.

- Partnership: Partners have unlimited liability, meaning they are personally liable for the debts of the partnership.

- Continuity:

- Company: A company has perpetual succession, meaning it continues to exist even if the shareholders change.

- Partnership: A partnership can be dissolved upon the death or withdrawal of a partner unless otherwise agreed upon.

(6 marks)

b) Disadvantages of Sole Proprietorship

- Unlimited Liability: The owner is personally liable for all the debts of the business.

- Limited Capital: It can be difficult to raise capital as the business relies solely on the owner’s resources.

- Continuity Issues: The business may not continue if the owner dies or is incapacitated.

- Limited Management Skills: The owner may lack the skills needed to manage all aspects of the business.

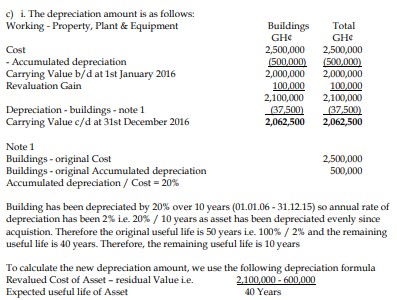

NOTE: Although the requirement did not ask of the restatement of the 2015 income statement, in

practice the income statement for 2015 will normally be restated to be comparable to 2016 as current

and previous year. This is same for the statement of changes in equity